According to the 2022 Small Business Credit Survey issued by the 12 Federal Reserve Banks, business loans and credit cards were the most popular sources of funding among surveyed firms.

Which one’s right for your business depends on certain qualifiers, such as how fast you need the financing and how much funding you need.

One type of funding will be better suited for your company than the other. Choosing the best fit is crucial to your short-term and long-term success.

Comparing Small Business Loans vs. Credit Cards

In comparing these financing options against the funding needs of your company, the choice may become clear. While there are pros and cons to every financing option, your company’s size, history and needs will determine the type that works best.

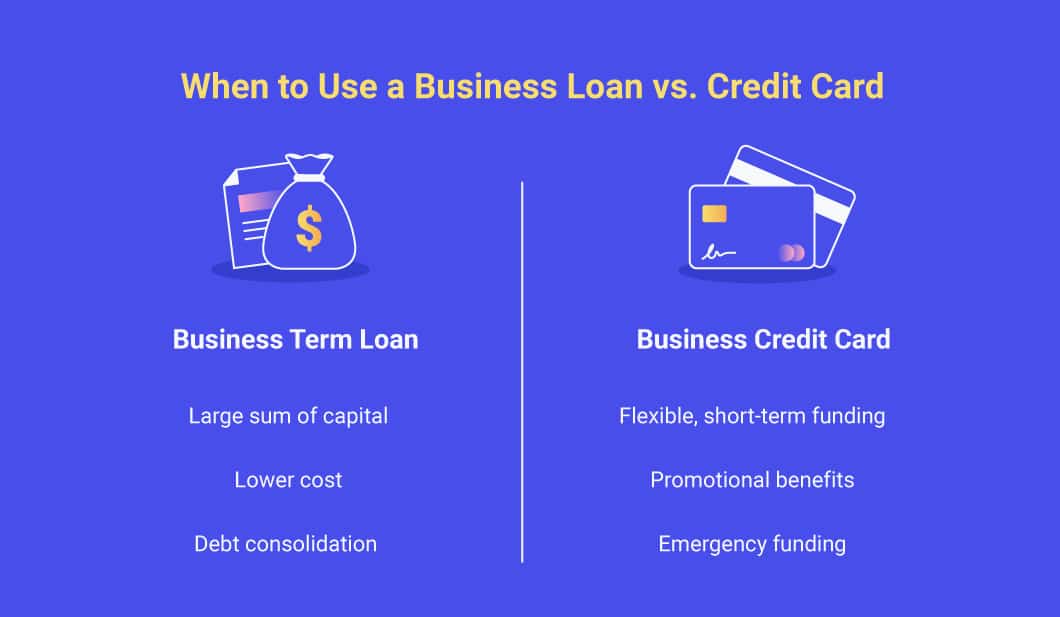

When Business Term Loans Are Best

Here are a few reasons to consider a small business loan vs. a credit card.

You Require a Large Lump Sum of Capital

If you need to fund a big project, such as a real estate purchase, business expansion or renovation, a term loan is likely a better fit. Loan maximums are often higher than credit cards, and what you’re approved for directly reflects your funding need.

You Want to Minimize Your Total Cost

Business term loans are often used for long-term projects or costly investments, while credit cards are best used for short-term or emergency expenses. That’s because credit card interest is calculated based on the average daily balance, which could make a credit card far more costly than a term loan if a borrower takes years to pay off a purchase. Compared to business term loans, credit cards also have recurring fees to consider, such as annual fees, and interest rates could fluctuate.

You’re Consolidating Debt

If you currently have several outstanding loans and are looking to roll all of your debt into a single loan as a method of debt consolidation, a business term loan will be a better fit. That’s because you could be eligible for a lower, fixed rate as well as longer terms than you’d find with a business credit card.

When Business Credit Cards Are Best

Now that you know a few reasons you might choose a business term loan over a business credit card, when might you choose the opposite?

Your Need Flexible, Short-Term Funding

Business credit card interest rates are frequently variable. As such, this type of financing isn’t often used for expenses you plan to pay off over the long term, as financing charges can make the purchase quite costly. But if you have a one-off purchase you can pay off quickly or recurring purchases you can pay monthly (e.g., subscriptions, utilities), a business credit card could be a great choice.

You’ll Take Advantage of Benefits

Sometimes, business credit cards offer 0% introductory interest rates as well as member rewards, such as cashback, hotel discounts, frequent flyer miles and purchase warranties. If these are appealing and beneficial to your business, a credit card might be a good fit.

You’d Like Fallback Funding

If you’d like a safety net for business capital, a credit card could be an option to consider. Once you’re approved, your credit line is available when you need it. You could go months without using it and then access it when a business emergency pops up.

Why Get a Business Credit Card?

When thinking about a business credit card vs. a business loan, consider that the former is ideal for offsetting periods of low cash flow. They’re best used to cover small expenses you can quickly pay back.

Business Credit Card Pros

- Credit Score Management: Having a business credit card potentially can increase your company’s credit score, which can help you qualify for a business loan.

- Continuous Funding: The repayment schedule and borrowing limit are fluid and ongoing. As long as you make on-time payments, you can have your credit line as needed and possibly increased too.

- Can Be Used Sparingly: Because your funding isn’t a 1-time disbursement but fluid, you only pay for what you spend. This can save you money if your expenses for a project are less than projected — and it can encourage thriftiness in your business operations.

- No Interest Charges Possible: You pay 0% interest if you pay off all your expenses on time. With a business loan, you pay interest on the financing regardless.

- Easy to Get: It’s easier to qualify for a business credit card than a business loan. Often, there’s less money credited than what you would receive in a business loan. Plus, the interest rate is higher. Keep in mind, a business credit card can be the stepping stone to a future business loan.

- Enticing Introductory APRs: Some business credit cards let you get a 0% APR in the first few months of carrying the card, so that monthly pay-off doesn’t start until later. This allows the line of credit to act as more of a loan for your business, which is especially helpful when cash flow is low.

Business Credit Card Cons

- Less Funding Available: The financing amount is smaller: Some credit lenders give 5 figures to companies that meet high qualifications, but even those amounts are smaller than larger business loans.

- Interest Rates Can Fluctuate: The interest rate rises sharply when the card isn’t paid back on time. This can cause you to lose money and make things difficult if you encounter cash-flow issues. After introductory offers, interest rates can increase significantly and change with the prime rate.

- High Fees Possible: There are several fees to keep in mind, such as annual fees, cash advance fees and late payment fees, among others. Be sure to read the fine print and understand what these are before proceeding.

- Negative Credit Score Impact: A business credit card potentially could hurt your credit score if you carry an outstanding balance or make late payments. This could hurt your prospect of securing a business loan in the future.

- Personal Guarantee Could Be Needed: While you likely won’t need to put up collateral for a business credit card, you may have to sign a personal guarantee, which means you’re liable if the business doesn’t pay its credit card bills.

Why Get a Small Business Loan?

Small business loans are an excellent funding option for stable companies with existing financial records and credit histories. That said, companies lacking a credit history may still acquire a loan by putting down collateral. Small business loans are a bigger commitment, but they’re the best way to secure large, long-term funding.

Small Business Loan Pros

- Large Sums Available: You can obtain larger sums of capital than what business creditors offer on lines of credit. Securing long-term funding in this way gives you what you need to focus on growth instead of worrying about where your next funding is coming from.

- Lower Interest Rates: Typically, there’s a much lower interest rate on business loans compared with business credit cards, which can charge higher interest rates on outstanding debt.

- Long Terms: Term loans can stretch as long as decades, in some cases, depending on the loan size and specific loan type. Rather than the payment installment being set on what you spend month-to-month, it’s based on a fixed payment schedule that ensures you can pay back the initial loan you took out in manageable chunks.

- Credit Score Strengthened: Business loans can build your company’s credit score if you make your payments on time and your lender reports to the credit bureaus. A good credit score can help you qualify for other funding sources.

Small Business Loan Cons

- Difficult to Qualify: It can be more difficult to qualify and get approved for a business loan as compared to a business credit card, particularly with conventional lenders. You’ll need to show prospective lenders your company’s tax returns and history of financial statements, which requires multiple years of history generating revenue. Lenders also want to see good credit scores, and if you don’t have one, you may have to offer collateral on the business loan.

- Collateral Requirement: In cases of secured business loans, you’ll be required to offer collateral, such as money or a vehicle. And if you end up offering collateral, you risk losing it.

- Long Application and Funding Timeline: Depending on the lender and specific loan type, it could take several weeks from the time of applying to funding as lenders review your application and credentials. If you need fast cash, you might consider an unsecured business loan, which is often quicker to fund, though repayment terms can be shorter than secured loans and interest rates higher.

Business Loan vs. Business Credit Card: Which Is Best?

Deciding on whether to take out a business loan or credit card will depend on your company’s size and funding needs. Think about your financing goals and weigh the risks of a business credit card vs. a loan.

Also consider the following:

- Financing amount

- Term length

- Interest rate

- Additional fees

- Total cost of financing

- Installment payments

- Collateral requirements