The answer is, it varies. After all, every business is different. What’s right for you might not be right for the company down the street. Some factors to consider include how long you’ve been operating, your revenue, cash flow and loan repayment terms, among others.

Here are 10 times when you should (or shouldn’t) get financing and what to weigh when asking yourself, “Should I take out a business loan?”

When to Get a Small Business Loan

In terms of when to get a small business loan, we don’t mean January or December. We’re talking about moments in your business’s path when you might be ready to apply for financing. Here are a few instances when getting a loan for your company could make sense.

1. During Good Times

Sure, there are loans out there to help you get through challenging financial periods, but that’s not the only time to turn to business financing. According to Forbes, “the best time to get a small business loan is before you desperately need one,” what the website refers to as proactive financing. This is when business is booming, your revenue is high and your cash flow is reasonably good. These are things lenders want to see.

2. If You Could Use a Buffer

If you’re a seasonal business owner, sometimes the slower months can make it challenging to get by. If you’re in a cash-flow crunch that history has shown is short-lived, business financing could provide a bridge of working capital to help you weather a temporary rough patch.

3. While You Have Solid Credit

Of course, we’ve all heard of bad credit business loans, but one of the best times to take out a loan is when your credit is good. Generally, the higher your credit score, the better terms and rates you’ll see when you apply for a small business loan.

4. If You Need to Invest in the Business

When you need to invest money back into your business to grow, a business loan could make sense. This could be the case when you’re looking to expand to a bigger location, invest in new equipment, buy bulk inventory or hire additional workers, for example.

5. When a Valuable Opportunity Knocks

Are you interested in featuring a new product line or partnering with another brand? Get your calculator and spreadsheets out. Forecast the return on investment (ROI) possible from an opportunity that’s calling your name. Find out if a small business loan could help you turn that opportunity into a profitable venture and increase revenue.

Related: Easily Calculate Business Loan ROI

-

Reasons Businesses Apply for Financing

According to the Federal Reserve Banks’ Small Business Credit Survey of 2022, reasons firms applied for financing included:

- Meet operating expenses, such as wages, rent and inventory (62%)

- Expand business, acquire business assets or pursue opportunities (41%)

- Refinance or pay down debt (30%)

- Replace capital assets or make repairs (29%)

When You Shouldn’t Get a Small Business Loan

Now that we’ve covered some instances when getting a small business loan could make sense, let’s look at when you should think twice.

1. When the Solution Doesn’t Match the Needs

Are you trying to get funding in the short term to help with what’s really a long-term challenge? For instance, maybe you’re in a cash business and find yourself struggling with company finances and think financing can help. If revenue is good but you find yourself experiencing one too many cash-flow issues, focus on getting your budget in check first (or consider applying for a loan to invest in a bookkeeper instead).

2. At a Time When You’re Overextended

Have you taken out multiple loans or reached the limit on an existing line of credit? While consolidating debt can be useful in some cases, if you have a pattern of stacking loans and mismanaging funds, you might be wise to consider another approach. Instead of applying for another loan and potentially digging an even deeper hole, learn to manage your current debt and finances better.

3. If You’re Uncertain About the Payoff of an Investment

When considering taking out a small business loan, it’s crucial to perform market research and conduct an ROI analysis. You probably already have all the benefits lined up in your mind, but you also want to be aware of any potential pitfalls. It’s also important to have an idea of when an investment will begin to be profitable and to what extent.

4. When You Want to Make a Costly Impulse Purchase

You think to yourself, I’ve got to have this, but ask yourself, do you really need that shiny object? Particularly if your business is just starting out, you might be better off initially steering clear of the glitz and glam and sticking to business essentials.

5. If You’re Looking to Fund Personal Expenses

Though it should go without saying, don’t take out a business loan to pay for individual needs. It’s a bad idea to mix personal and business finances, much less personal and business debt. Some business lenders even have explicit statements in their contracts that prohibit use of funds on nonbusiness-related expenses.

Business Loans Pros and Cons

The pros and cons of business loans can be broken down by many factors, including lender, loan type and repayment terms. That said, here’s an overview of general ones to keep in mind.

Pros

Retain Control of Your Business

Unlike investors who own a stake in the business, lenders don’t. You decide how to run your company. Additionally, unless specified in the terms of your lending agreement (e.g., commercial real estate loan, equipment loan), you can often spend your loan proceeds on virtually any business-related expense. Along the same lines, because you’re not tapping into an investor, you don’t need to give away equity. You stay in control of your company.

Build Your Credit

In some cases, taking out a small business loan is a way entrepreneurs can build business credit. If your lender reports your payments to credit reporting agencies, you can build your credit by making payments on time and not taking out more financing than you can handle.

Get Through a Slow Season

Ebbs and flows are common in business. When entrepreneurs experience short-term lulls, a working capital loan can help. Business owners can leverage financing to maintain the status quo and get through cash-flow interruptions.

Cons

Shortages Can Arise

On the flip side, if your payments are too high and too frequent, you might find yourself with a cash-flow shortage, particularly if revenue declines. When you’re seeking financing for your business, be honest with yourself and your budget.

Ask yourself what you really need, and what payments your business can truly afford to make. Also, be clear on the terms of any financing offers you receive, including any up-front fees, interest rate, payment frequency and repayment term.

Risk Equals Less Competitive Terms

When lenders evaluate loan applications, they evaluate risk. Factors such as low credit score, short credit history and outstanding debt are considerations that play into creditworthiness.

Higher risk can lead to higher interest rates as well as shorter repayment terms. The higher the interest rate, the more your loan will cost you.

Debt Can Affect Business Valuation

Bank loans are counted as a business liability. Because they’re shown on a company’s balance sheet as a liability, a business’s valuation could be affected.

Risks in Taking Out a Business Loan

Personal Risk

If you have trouble making payments or default on your business loan, your personal credit score can take a hit. What’s more, if you give a personal guarantee, you’re also responsible for the business loan. This could affect plans you may have for financing a personal vehicle, purchasing a house, refinancing a mortgage and more.

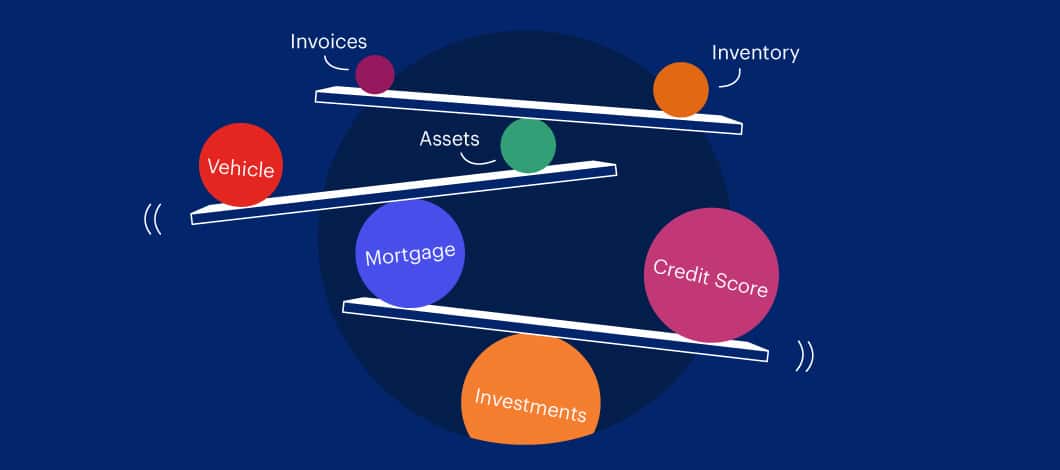

Collateral Obligation

In contrast to unsecured loans, if you’re applying for a secured business loan with a conventional lender, such as a bank, you’ll likely need to provide collateral. Examples of collateral include real estate, inventory, vehicles, invoices and investments. If you default on a loan secured by collateral, the lender has the right to recover its loss by taking ownership of the property you pledged.

Blanket Lien

In some cases, lenders can file a blanket lien to protect themselves in the event of default. This is common with SBA loans and alternative financing. As opposed to specific collateral, blanket liens allow financing companies to lay claim to most or all of a business’s assets.

Related: Conventional vs. Alternative Lending

What to Consider Before Applying for a Business Loan

When you’re asking yourself, “Should I take out a small business loan?” consider the many factors at play as well as the pros and cons of business loans. Additionally, think about your company profile from a lender’s eyes and how hard it could be to take out a loan. Keep in mind that time in business, revenue, cash flow and credit score can impact the loan type, amount, interest rate and terms for which you’re able to qualify.