If you operate a black-owned business or any other minority-owned business and need a loan, there are financing opportunities available.

What Are Minority Business Loans?

Small business loans for minorities are intended to give socially or economically disadvantaged groups access to business financing. While many funding options aren’t specifically labeled for minorities, there are programs and organizations that help connect minority business owners with financing opportunities.

Let’s take a look at what small business loans for minorities are available, how to qualify for them and the additional resources that can connect your business with the funding and guidance it needs to flourish.

Is Your Business MBE Certified?

Many organizations will require you to be a certified Minority Business Enterprise (MBE) or Disadvantaged Business Enterprise (DBE) to be eligible for black-owned business loans, grants or other resources. The main provider of these certifications is the National Minority Supplier Development Council (NMSDC). Their MBE program qualifies you as a DBE and is recognized nationwide by suppliers, both public and private.

To qualify, your business must:

- Be at least 51% owned by 1 or more members of an approved minority group

- Have day-to-day operations and decision-making handled by minority owner(s)

- Be a for-profit business

- Be located in the territorial U.S.

Best Small Business Loans for Minorities: 7 Sources

| Financing Resource | What It Does |

| SBA Microloans | Small business loans, up to $50,000, that can be used for minority startup enterprises |

| SBA Community Advantage Loans | Provides credit, as well as management and technical assistance, to for-profit businesses in underserved communities |

| Accion Network | A network of lenders aiming to help minority business owners |

| Union Bank | Offers both secured and unsecured loans for minority-owned businesses |

| BCF Direct Lending Program | Makes loans up to $1.125 million for maximum 7-year terms |

| BCF Loan Participation Program | Similar structure to SBA 504 loans, but can be used for refinancing |

| Indian Loan Guarantee Program | Facilitates lending to American and Alaskan native individuals and tribes who otherwise haven’t qualified for conventional funding |

| State and Local Programs | Some lending programs are available to respective communities (e.g., the Office of Hawaiian Affairs Mālama loans) |

Related: Business Loan Requirements

1. SBA Microloans

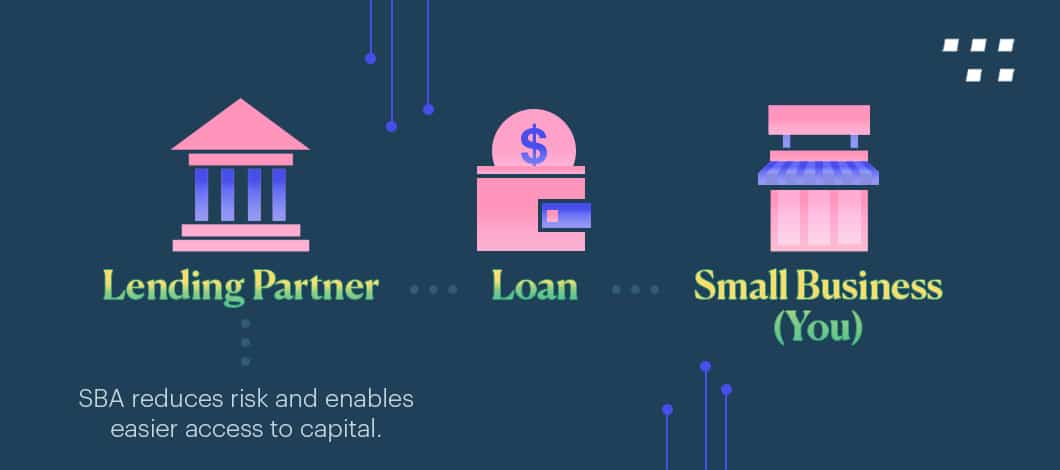

Through the Small Business Administration’s (SBA) loan programs, the SBA guarantees a percentage of the funding for small businesses. SBA loans are good options for minorities who don’t qualify for traditional bank loans and are an excellent choice for minority owners facing financial challenges.

While there aren’t any restrictions regarding who can apply for SBA microloans, this program is particularly beneficial for women, veterans, economically disadvantaged or minority business owners who have recently launched their ventures.

Microloans are issued by third-party lenders, which in most cases, are nonprofit, community-based organizations. While the maximum funding amount available to applicants is $50,000, the average loan is $14,000. You can expect an interest rate between 6%-9%.

Microloans can be used for working capital, inventory, supplies or purchasing machinery, among other purposes, but they cannot be used for real estate purchases or debt refinancing.

If you’ve been seeking black- or minority-owned business loans for your startup, microloans can help entrepreneurs who might have limited financing options when opening a new company.

2. SBA Community Advantage Loans

The SBA Community Advantage Loan Program opens access to financing options that some minority business owners might not otherwise qualify for.

The program encourages local lenders, nonprofits and even mission-focused organizations to issue SBA 7(a) small business loans for female minorities, veterans and other members of underserved communities.

The SBA typically considers inner-city and rural areas and any low- to moderate-income community that’s “underserved.” If your business has at least 50% of its employees residing in an underserved area, you could qualify for the Community Advantage Loan Program.

The SBA guarantees up to 85% of the amount issued (maximum of $250,000), making this an excellent option for you if you’ve had trouble qualifying for conventional term loans.

Term length maximums are 10 years for working capital and equipment and 25 years for commercial real estate.

Interest rates are comparable to 7(a) program loans, with maximum rates at 9.25%.

Note that this is a pilot loan program that will end Sept. 30, 2022, unless it becomes part of the SBA’s permanent slate of loans.

3. Accion Network

The Accion Network’s goal is to distribute small business loans for minorities, and other funding, across the United States. More than 60% of Accion Network’s borrowers are part of minority groups.

This nonprofit organization offers affordable, flexible funding options to businesses across industries. You can apply for microloans and qualified borrowers can receive more substantial amounts.

Accion offers loans for everything you need, from working capital to renovations.

They’re an excellent option for startups, as well.

4. Union Bank

Union Bank’s Business Diversity Lending Program offers up to $2.5 million in loans for minority business owners.

The program is designed to help small minority businesses finance projects of all sizes. Qualifying businesses must have been operating for at least 2 years and have annual sales of less than $20 million.

Union Bank offers both secured and unsecured loan options with fixed or variable rates. Your creditworthiness will determine your financing amount and terms.

5. Business Consortium Fund

The Business Consortium Fund (BCF) is a registered CDFI that offers minority business loans. They have 2 programs open to any certified Minority Business Enterprise seeking funding.

BCF Direct Lending Program

The BCF will often directly lend to businesses. They offer term loans and lines of credit, ranging from a minimum of $75,000 to $500,000, although loans up to $1.125 million will be considered on a case-by-case basis.

Loans reach maturity in 7 years, making these a good loan option for minority owners who need a medium-sized term loan.

BCF Loan Guaranty/Loan Participation Program

Like SBA loan programs, the BCF guarantees part of your funding if you have trouble acquiring financing from traditional lenders. Their involvement, dubbed the Loan Guaranty/Loan Participation Program, provides a credit enhancement by covering a portion of the funding.

Consider BCF loans for minority business owners if you need to finance equipment or invoices, or need a quick boost in working capital.

6. Indian Loan Guarantee Program

The Indian Loan Guarantee Program (ILGP) helps American Indian and Alaskan native tribes or groups obtain funding from various lenders, excluding credit unions, by providing guarantees or insurance for minority business loans. These guarantees can help native business owners secure financing at reasonable rates, which might otherwise be unattainable.

These are the requirements to qualify for the ILGP:

- Be an enrolled member of an American Indian or Alaskan Native tribe or group

- Be an American Indian or Alaskan native group or tribe

- An American Indian or Alaskan Native tribe or group must have 51% ownership of the financed business

- The financed project should benefit a reservation or tribal service area’s economy

- The borrower must invest 20% equity in the project

ILGP-secured funding can be used for operating capital, lines of credit, construction and equipment purchases, among other projects.

7. State and Local Programs

Helping business owners obtain financing to grow their companies is one way state and local governments can ensure their respective economies thrive.

There are myriad programs available, and the easiest way to find one for your business is to search the web for (your state’s name) and “minority business loans.”

One such program is the Pennsylvania Minority Business Development Authority (PMBDA). The PMDBA provides low-interest minority business loans that can be used for different purposes, including working capital, building construction and renovation projects. The authority will finance up to 90% of approved projects.

Another program is New York’s Accompany Capital, which provides small business loans, credit-building loans and microloans to minority business owners.

SBA Loans for Minorities

The following loan options aren’t specifically geared toward minority business owners. However, these financing packages are helpful if you haven’t qualified for a conventional loan.

Standard SBA 7(a) Loans

SBA 7(a) loans offer up to $5 million for borrowers, meaning you can use them for large or small projects. The SBA guarantees up to 85% of your loan, reducing the risk for lenders and opening access to affordable long-term financing to previously disqualified candidates.

Interest rates depend on your creditworthiness but are generally not far from what banks offer. Terms range from 7-25 years, depending on the amount you borrow and the intended use.

Requirements vary by lender. For example, to qualify for an SBA 7(A) loan through Fast Capital 360, you’ll need to have:

- At least $50,000 in annual revenue

- At least 2 years in business

- A credit score of 650+

Although they’re flexible, it takes a few weeks to a month to receive approval, and even longer to get the funding.

SBA Express Loans

With many SBA loans, you’ll have to wait several weeks before learning whether your application will be approved. In contrast, SBA Express Loans can have capital in your bank account in as little as 30 days.

However, in exchange for the expedited process, the interest rates are slightly higher, and you’ll have a lower maximum borrowing potential. You can borrow up to $350,000 over a 5- to a 10-year term.

The SBA guarantees only 50% of these deals, making them riskier for lenders, which can impact your terms and chances of approval.

SBA 504/CDC Loans

The SBA 504 loan program is excellent if you need to purchase fixed assets such as equipment, commercial trucks and real estate.

These SBA loans are partially funded by Certified Development Companies (CDC), nonprofit partners of the SBA that aim to help build America’s small business infrastructure.

Here’s the funding breakdown:

- Bank loan: 50% (or more)

- CDC loan: 40%

- Borrower’s down payment: 10% (or more)

The CDC-backed portion of the loan is capped at $5 million. There is no cap for the bank-serviced part of the loan. In general, interest is not much higher than what banks offer, ranging from 2.2% – 2.4%, and terms go up to 25 years for the CDC portion of the loan.

Find Business Loan Options In Minutes

Small Business Loans for Minorities with Bad Credit

You can obtain minority business loans even if you have bad credit or scant credit history.

Banks and alternative lenders have options that can connect you with the funding you need for your business.

Short-Term Loans

Short-term loans, which are abbreviated versions of conventional term loans, are a more accessible path to financing minority business loans for applicants with less-than-stellar credit.

Like a conventional term loan, you’ll finance a project with a lump sum of money. You’ll then repay the principal, with interest, according to an agreed-upon schedule.

While some term loans can be repaid over decades, many short-term loans reach maturity in 18 months or fewer.

Small business loans for minorities with bad credit are seen as riskier, so lenders require shorter, more frequent repayment schedules — sometimes with weekly or daily payments — and higher interest rates. The maximum funding amount can also be smaller than what you would get with a conventional term loan. For example, with Fast Capital 360’s lending partners, borrowers can be approved for $500,000.

Business Line of Credit

With a business line of credit, a lender approves you for a funding amount that you can draw from to finance your business needs. You repay and pay interest on only the capital you’ve used. Once what you borrowed from your business line of credit is repaid, you can again withdraw funding.

Merchant Cash Advance

A merchant cash advance (MCA) isn’t a loan, but funding provided against future sales or projected revenue. Borrowers could be advanced up to $500,000 through Fast Capital 360’s lending partners. Factor rates can start at 1.10 and funding can be received the same day as approval.

There are 2 types of MCAs — traditional and automated clearing house (ACH).

Traditional

In a traditional MCA, lenders are repaid in daily or weekly installments through a percentage of sales that are “held back” from the borrower. The holdback percentages can range from 10% to 20%.

ACH

With ACH MCAs, repayments are fixed amounts that are withdrawn from a bank account in daily or weekly installments. The repayment amounts don’t vary according to sales totals.

Small Business Startup Loans for Minorities

Acquiring funding can be difficult when you don’t have an established business credit history or current revenue reports. However, even up-and-coming entrepreneurs can obtain business financing with the following options:

- SBA microloans

- Accion Network lending

Other financing options include the following:

- Personal Loans: If you have a strong personal credit score and history, a personal loan can help fund your new venture if you can’t qualify for traditional business lending. Note that these loans might be better if you’re experiencing a smaller financial gap. Personal loans are often approved for small funding amounts — 4 or 5 figures vs. 5, 6 or even 7 figures with business lending — and shorter terms, which can be a maximum of 7 years for personal loans vs. 25 years for some business loans.

- Business Credit Cards: A business credit card helps you build your business credit history and is a good option for business owners who are unable to be approved for traditional financing. You can also take advantage of initial 0% APR offers. However, like personal loans, note that total spending amounts are often smaller compared to what you can get from business financing.

Minority Business Loan Requirements

Small business loans for minorities are designed explicitly for racial and ethnic minorities, as well as socially or economically disadvantaged individuals.

Although some financing options target a specific minority group, most provide small business loans for entrepreneurs in the following racial/ethnic groups:

- African-American

- Asian-American

- Hispanic-American

- Native American

- Pacific Islander

- Alaskan Native

While some of these loans have unique requirements for borrowers, many programs have similar qualifications. In general, certification as a Minority Business Enterprise (MBE) or Disadvantaged Business Enterprise (DBE) is enough to pre-qualify for minority business loans.

Applying for Minority Business Loans

After choosing a lender, you’ll submit paperwork and financial documents to apply for small business loans for minorities.

While minority business loans vary regarding their required documents, in general, you’ll need to gather the following before applying:

3 years of:

- Business and personal tax documents

- Revenue statements

- Profit and loss statements

- Recent bank statements

- Balance sheet

- Voided business check

Traditional Lenders

Traditional lenders such as banks and credit unions will usually have lengthier processes; obtaining a minority business loan could take weeks or months depending on your lender. While each institution varies in regard to specific practices, you might have to complete several steps before your application is approved, including meetings with the lender’s representatives and a site visit to your business.

Alternative Lenders

Alternative, or online, lenders’ application process is usually online only, as it is for Fast Capital 360. The entire process can take only minutes if you have all of your relevant business documents and information ready for entry or upload. Once lenders have your information, applicants know within days whether their financing request is approved or denied. If approved, you can often receive funding on the same day.

Related: How It Works

Additional Resources for Minority Business Owners

Outside of funding, there are programs and groups that can help minority business owners through mentorship, networking and special consideration for contracts. There are many groups that you can turn to for help securing your small business’s financial and strategic future.

Minority Business Development Agency (MBDA)

The MBDA works to help minority-owned businesses find the capital, contracts and markets they need to succeed. They focus on serving people and building economies of communities with large minority populations.

MBDA offers technical, management and marketing training to build a better strategy for your business’s future.

If you need minority business loans or other funding, they’ll help you find lenders. Their network of business centers is available to all minority business owners.

SCORE

The Service Corps of Retired Executives (SCORE) offers you the opportunity to learn how to run your company from successful entrepreneurs and former executives.

Mentors with SCORE guide you through all levels of business ownership. They can help you navigate the startup phase, expansion and even teach you how to obtain small business loans for minorities.

The nonprofit also holds conferences and workshops that, for a small cost, offer you training as well as an opportunity to network with mentors and fellow entrepreneurs.

Grants

There are numerous grant opportunities for minority business owners to obtain funding. For-profit businesses and nonprofit organizations offer grants, as do federal and state governments. Unlike with minority business loans, grant recipients don’t have to repay their awarded money.

The funding amounts and application requirements vary; some grants also offer mentorship and publicity opportunities.

Business Financing for Minorities: Frequently Asked Questions

Are There Small Business Loans for Female Minorities?

Female minority business owners are eligible for the funding and resources available to all applicants from minority communities as well as female business owners. While no financing packages are labeled exclusively for female minority business owners, there are lender programs and networks that help connect women minority business owners with the funding they need.

What are Low-Interest Business Loans for Minorities?

Interest rates are influenced by a variety of factors, including your own credit scores and your business’s financial health. If you have a good to excellent credit score, lenders can see you as less of a risk and improve your chances of qualifying for low-interest financing. However, if you haven’t been able to qualify for traditional business financing, SBA 7(a) and 504 loans are your best option for low-interest business loans for minorities, with rates ranging from below 3% to slightly less than 10%.