If your business is experiencing a cash crunch and you need funds quickly, what are your options?

Conventional or government-backed loans can take time to process and the application can be rigorous. It may be weeks or months before you receive the money.

Short-term lending offers businesses a convenient application process and quick access to funds. In spite of the potential for higher costs, short-term credit can help your situation. Learn how.

What Is Short-Term Business Lending?

With short-term business lending, a lender provides you with working capital financing that you pay off within a short timeframe. Specifically, these business loan terms may give you up to 18 months to repay your funds.

As with conventional loans, you’ll pay back your loan amount plus interest and other fees. Short-term financing differs from standard loans because it requires less paperwork or documentation.

Short-term loans are meant to be paid off quickly. Indeed, short-term loans may offer reasonable rates if you pay off the loan within months, though.

Higher annualized interest rates are seen the longer financing terms extend. For example, if you take a year to pay, some short-term lending interest rates may equate to high double-digit annual percentage rates (APR).

Related: Short-Term Loans: Why APR Is the Wrong Metric

When Do Small Businesses Use Short-Term Loans?

Most short-term business loans help companies pay their bills during a financial shortfall — from operating expenses to payroll. A company may choose a short-term loan to avoid paying interest payments over many years, which increases lending costs.

Reasons why small businesses may use a short-term loan include:

- Seasonal business inventory

- Seasonal cash-flow issues

- Startup expenses for a new project

- Immediate business opportunity

- Emergency repairs

- Emergency equipment replacement

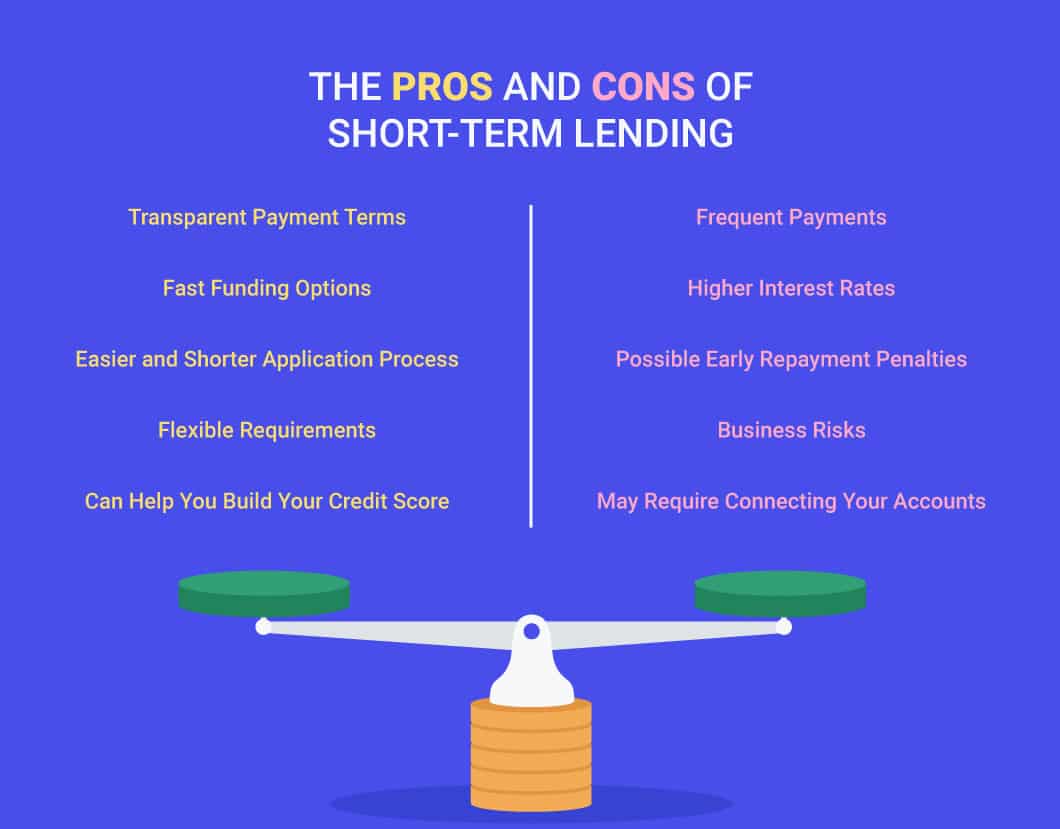

Pros of Short-Term Lending Options

There are several advantages of a short-term loan. Of course, the biggest is that it can fix pressing financial problems, from paying employees to covering expensive repairs.

However, for small businesses, there are other benefits to short-term lending solutions, including:

Transparent Payment Terms

Before accepting a loan, you’ll receive short-term lending rates applicable to your situation and funding type. You also get a simple payment schedule. Your financial provider may offer daily, weekly or monthly payment options.

Fast Funding Options

Unlike long-term business loans, you can receive short-term funding within 24 to 48 hours. Same-day business loans can help you pay your supplier for crucial inventory or get equipment repaired so you can reopen your doors quickly.

Easier and Shorter Application Process

Short-term lending applications usually take place online. Depending on the loan type, you may not need extensive documentation required for long-term financing options.

Instead, you share pertinent details on your digital application and may be prompted to connect your accounting software or bank account for quicker loan determination.

Flexible Requirements

To get a conventional business loan, you may face more restrictions. For example, many lenders require good to excellent credit scores, a certain number of years in business and a high minimum revenue figure.

However, short-term lending solutions may work for business owners with lower credit scores or even bad credit. You can work with short-term lenders to find a financing option that doesn’t require collateral or provides funds based on incoming revenue instead of how much money you have in the bank.

Can Help You Build Your Credit Score

Many times, short-term financing a borrower takes out isn’t reported to the credit bureaus. While this means your payments aren’t reported, it also means the amount of funding you receive doesn’t reflect as added debt on your credit report, which can be a benefit to you if you’re working to improve your credit.

Additionally, you can use the funds you’re approved for to pay down your existing business debt and start rebuilding your credit score. Paying down your debt could help improve your credit score within months.

Cons of Short-Term Lending Solutions

Before selecting a short-term loan, it’s vital to ensure you can meet repayment stipulations. A failure to do so may result in steep fines and larger payments that are difficult to pay off fully. Here are some of the challenges common of short-term loans.

Frequent Payments

Instead of monthly loan payments, a short-term loan requires daily or weekly payments. Although automating payments helps you save time, you need to have the funds in your account for recurring payments.

Higher Interest Rates

Short-term financing comes with higher rates than longer term loans. If you pay them off quickly, you can save money. But if you take a full year or more to pay off, then the interest rate could be higher than getting a cash advance from a credit card.

Possible Early Repayment Penalties

Some lenders charge extra fees if you pay your loan off early. This can drag out your loan terms, forcing you to pay more over an extended period.

If a lender charges early repayment penalties, then look for financing companies that don’t charge these fees.

Business Risks

The increased financial pressure from high-cost short-term credit poses a risk for business owners. You must prioritize paying off a short-term loan and put other projects on the back burner.

If you can’t recoup your money quickly, you may feel inclined to take out another loan or extend your loan terms. Doing so can put you in a position where your cost of debt is more than your revenue.

May Require Connecting Your Accounts

Many short-term lending solutions use your accounting program or online banking information during the application and repayment process.

Although doing so helps you get approved and paid quicker, not everyone wants their accounts connected to a lender.

Examples of Short-Term Commercial Lending Solutions

There are several types of short-term lending solutions. Each offers different financing terms and may work better for specific situations.

Before applying for business financing, consider your options. Look for terms that fit your circumstances and ensure the return on investment makes sense for your business.

Short-Term Business Loans

Use a short-term loan to cover emergency expenses or income shortfalls. These loans require daily or weekly payments. Repayment term periods typically are 3 to 18 months.

Short-term business lending options help you:

- Finance up to $500,000

- Cover operating expenses (e.g., payroll, rent)

- Stay afloat during a slow season

Merchant Cash Advance

With a merchant cash advance (MCA), you get an advance on your future sales. Business owners usually pay daily or weekly payments until the advance and fees are paid in full.

MCAs offer:

- Payment terms of 3 to 24 months

- Up to $500,000 or more in financing

- Factor rates instead of interest rates

- Funds could be available the same day as approval

Business Lines of Credit

A business line of credit can be a flexible solution for ongoing cash-flow concerns or emergency expenses. You only pay interest on funds you use. Additionally, with a revolving line of credit, once you pay back the borrowed amount, then the full funds are available for use.

A business line of credit:

- Doesn’t incur interest until you use the funds

- Often 6- to 24-month repayment terms are available

- Typically incurs a draw fee each time funds are accessed, often 1%-3%

Working Capital Loans

Cover operating or project-based expenses with a working capital loan. Working capital loan is an umbrella term that encompasses several types of short-term commercial lending options, including cash advances, short-term loans and lines of credit.

A working capital loan often has the following characteristics:

- Helps bridge cash-flow gaps

- Daily or weekly loan payments

- Repayment timelines of 3 months to 5 years

Accounts Receivable Financing

A popular product in the short-term lending market is accounts receivable financing, sometimes referred to as invoice financing. With this type of financing, a lender advances you a percentage of your outstanding invoices. Once your customer pays, your lender takes out fees, and you receive the rest of the funds.

This short-term loan solution provides:

- No limits on use of funds

- Same-day access to funds possible

- Often 70%-90% advance on your outstanding invoices

- Factor rates instead of interest rates, often calculated weekly

Is Short-Term Business Lending Right for You?

Short-term loans are offered through banks as well as alternative lenders. Weigh the pros and cons of short-term business lending options and offerings from various providers. The best financing solutions provide the funds you need with a return on investment that makes sense for your business.