Apply to multiple lenders with just one applicationLearn More

A borrowing base measures how much you can borrow with an asset-based loan. It’s based on a percent of your collateral’s value.

Learn more about:

What a borrowing base is

What types of loans use borrowing-base considerations

How to tally up your collateral with a borrowing base certificate

How to calculate your borrowing base

Borrowing Base: A Definition

The borrowing base is a metric commercial lenders use to measure the value of assets a business can pledge as collateral for an asset-based loan.

This number determines how much the lender can afford to risk loaning you, so your borrowing base is also equivalent to the amount you can borrow from that provider. The higher your borrowing base, the more your lender is willing to loan and the more favorable terms and rates they may extend.

Borrowing-base calculations take into account any types of collateral you can pledge, including:

Real estate

Equipment

Inventory

Accounts receivable

The borrowing base will vary with changes to the value of assets. As more assets become available, the borrowing base can be reconsidered.

Borrowing bases are important because lenders have no guarantee of recovering the full value of a small business owner’s collateral in the event of loan default. For instance, real estate or inventory may prove slow to sell, equipment may depreciate or customers may fail to pay what they owe.

What Is a Borrowing Base Advance Rate?

Because of this uncertainty and risk, borrowing base formulas calculate the value of your collateral based on a percentage rate rather than the total value of your assets. This rate is known as a borrowing base advance rate or discount rate.

Advance rates can vary by lender as well as by the type of collateral pledged. To calculate your borrowing base, you’ll need to know your lender’s advance rates for the types of collateral you’ve committed.

Once you know the value of your collateral and the percentages for your lender’s advance rates, you can calculate your borrowing base. Multiplying the value of each type of collateral by its corresponding rate and then summing up the totals for all types of collateral yields your borrowing base. The result represents the cap on the amount your lender is willing to loan you.

For example, let’s say your collateral has a value of $100,000 and your financing provider offers you a 75% advance rate. That means the lender is willing to offer you $75,000.

Note, because financing providers can have different advance rates, your borrowing base can vary from lender to lender. One may be willing to extend you more than another based on the same collateral.

How to Calculate a Borrowing Base

To calculate your borrowing base:

Take the value of the assets you’re pledging as collateral (accounts receivable, inventory, equipment, etc.) and multiply by your lender’s advance rate

Add values together

When calculating accounts receivable, the standard procedure is to use what’s called an accounts-receivable aging report. This report breaks your accounts due into ranges based on how far they’re past due. Asset-based lenders typically require you to exclude accounts that are more than 90 days past due, and they may have other restrictions. This can vary by lender, so check requirements before completing your borrowing base certificate.

When calculating the inventory value, you will need to subtract any ineligible inventory before multiplying by your lender’s advance rate. Ineligible merchandise can include:

Inventory you have stored where you don’t pay the supplier until after the goods are consumed (consigned inventory)

Inventory that is near the end of its lifecycle and not expected to be sold (obsolete inventory)

When calculating the value of equipment, use the equipment’s current value that factors in depreciation, not the original value of the equipment. Your lender will also want you to factor depreciation into any ongoing borrowing base certificates.

Borrowing Base Formula

These guidelines can be simplified into a formula:

B = [(AR)*(rAR) + (I)(rI) + (E)*(rE)]

Where:

B = borrowing base

AR = accounts receivable valuation (after any adjustments for ineligible accounts)

rAR = advance rate for accounts receivable

I = inventory valuation (after any adjustments for ineligible inventory)

rI = advance rate for inventory

E = equipment valuation (after depreciation factored in)

rE = advance rate for equipment

Borrowing Base Example Calculation

To illustrate how this formula might be applied, consider a borrowing situation where:

This means the lender could fund the borrower a maximum of $1,060,000 against the borrower’s combined collateral.

If an existing loan is in place, you’d also need to subtract the current loan or line of credit amount from the eligible borrowing base. This would give you the available funding amount.

For instance if you had a loan of $100,000, you’d subtract this from $1,060,000. This would leave $960,000, which is the total amount of funding a lender would be willing to extend to you.

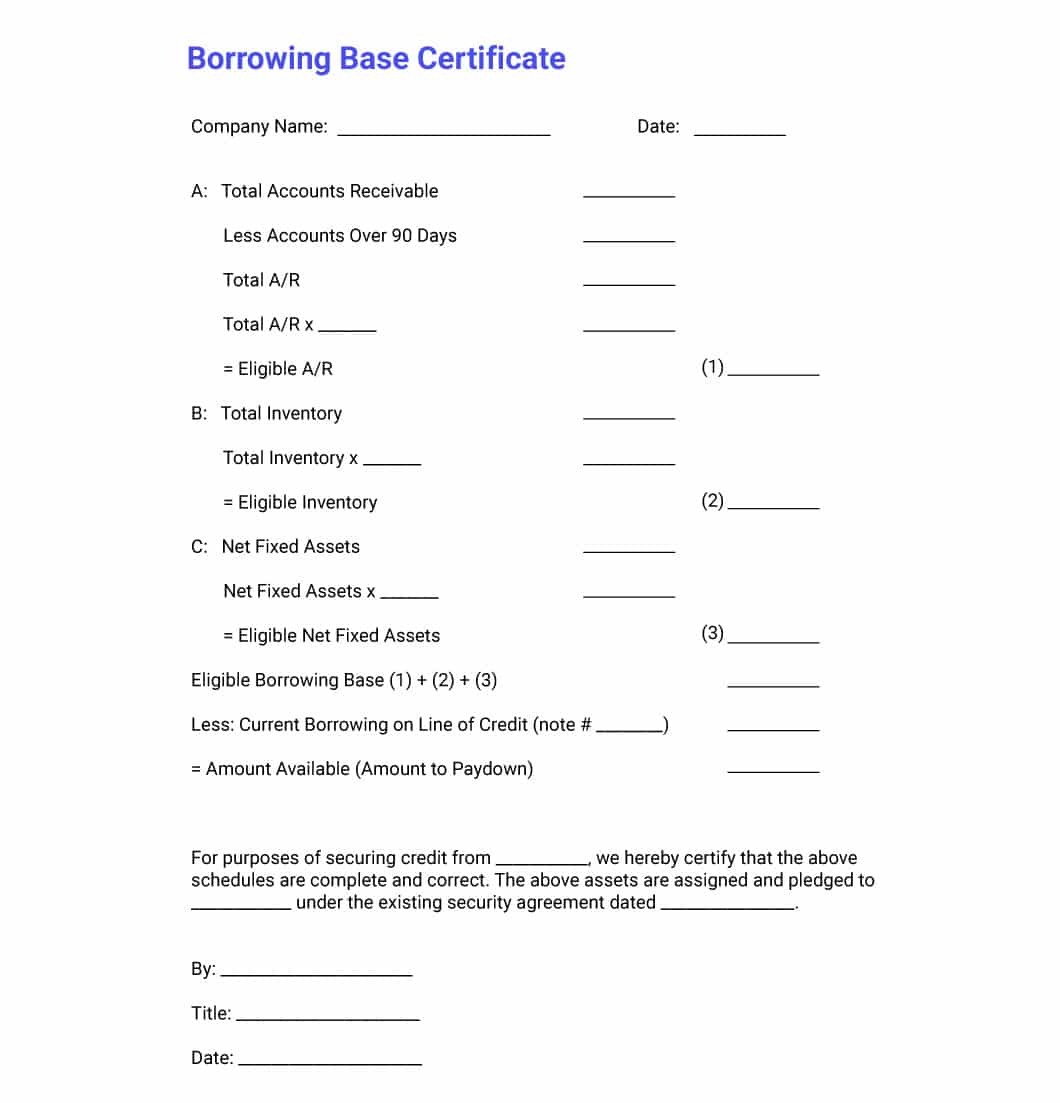

A borrowing base certificate form is a document lenders typically require you to submit when applying for an asset-based loan or another form of financing. It identifies your available assets as collateral and determines the value of those assets after your lender’s advance rates. This provides the information needed to calculate your borrowing base.

In many cases, lenders prefer to have the information on a borrowing base certificate form verified by a third-party professional who can attest to the accuracy of figures. If your borrowing base certificate isn’t directly drawn up by a professional, your lender may require an audit of the information.

Since the value of your assets can change over time, lenders often require the information on borrowing base certificates to be reviewed and updated periodically, sometimes monthly. This may require ongoing audits. If the value of your collateral drops below the level of your original borrowing base, you may need to repay part of your loan to bring your debt back within the parameters set by your lender.

Borrowing Base Certificate Format

The format for a borrowing base certificate form generally contains a few key features, which can vary with the type of collateral involved and with your lender’s policies.

Key information includes:

Name of the borrower

Date of the certificate

Sections summarizing each type of asset you’re offering as collateral, with each section covering:

Date

Value of inventory

Subtractions for any ineligible amounts

Value after advance rates have been applied

Summary tallying the value of all your asset types after advance rates have been applied

Adjustments for any debt balances

Total borrowing base after adjustments

Signature block with date

Keep in mind, your lender may supply you with a form for your borrowing base certificate. A third-party professional, such as an auditor or a lawyer, can also provide you with a customized form. Alternatively, you could use a borrowing base certificate template, such as the one below.

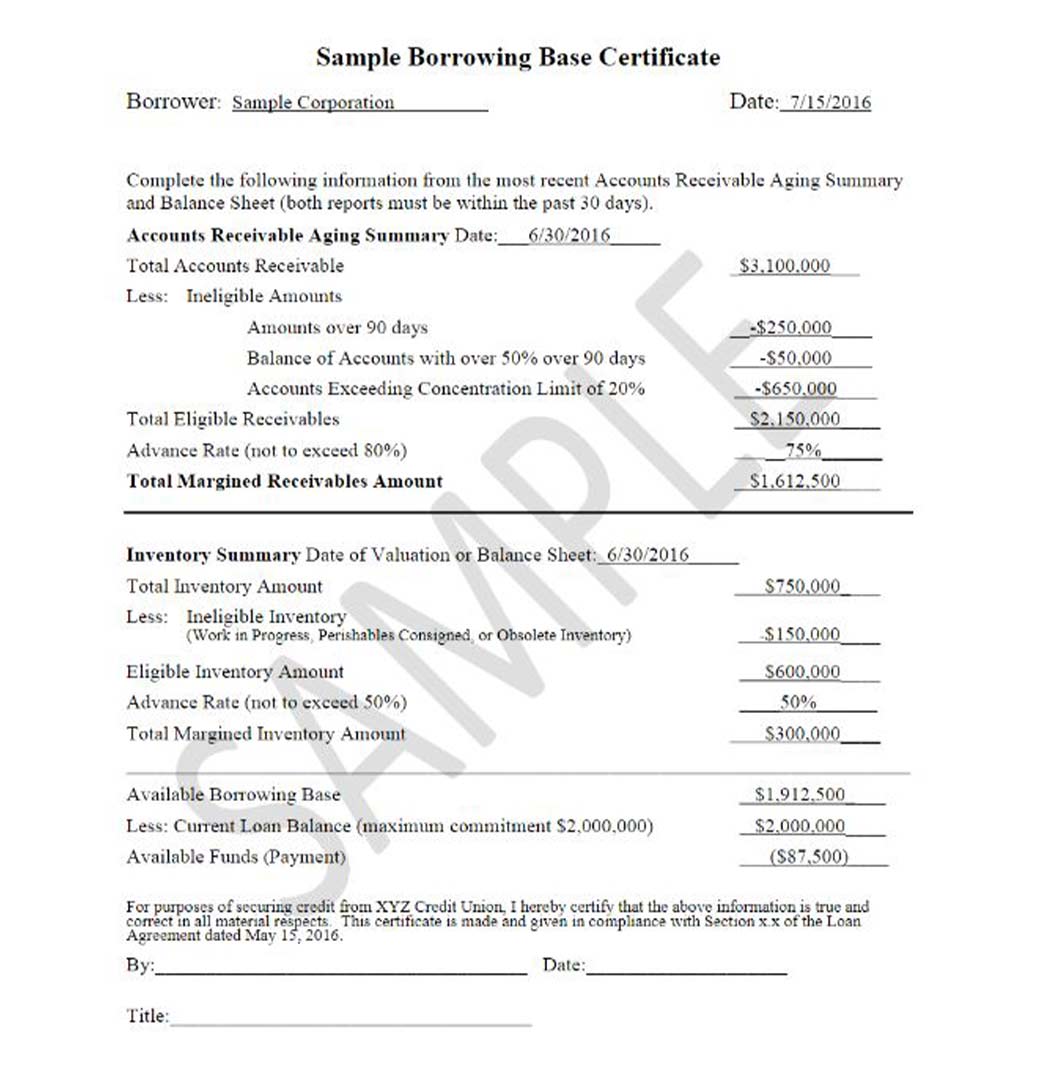

Sample Borrowing Base Report

Additionally, here’s an example of a completed borrowing base report:

Source: PDFFiller

Types of Financing Using the Borrowing Base Metric

In general, a borrowing base may enter into the picture with any type of financing where physical or financial assets are pledged as collateral. While several tangible assets may serve as collateral for purposes of calculating the borrowing base, these are the most common types of financing that employ borrowing base lending calculations:

Accounts receivable financing

Inventory financing

Equipment financing

Real estate financing

Accounts Receivable Financing

This type of financing is based on the value of unpaid invoices your customers owe you. You sell your lender your unpaid accounts receivable, and they give you an advance based on a percentage of the value of your outstanding receipts. They then collect the total value of your receipts from your customers and pay you the rest of the money, minus a fee that serves as your provider’s cut for their services.

Inventory Financing

With inventory financing, your inventory serves as collateral for a line of credit or short-term loan. Your lender provides you with funds based on a percent of the value of your stock. You must then repay the money according to the terms of your line of credit or loan agreement.

Equipment Financing

In equipment financing, you borrow money to lease, buy or upgrade equipment. The equipment being financed serves as collateral, making this type of financing self-collateralizing.

Real-Estate Financing

The borrowing base is also used in real-estate loans and equity lines of credit. Equity is the amount of money you’d receive after paying off your mortgage if you sold your property. It’s calculated by taking the current fair market value of your property and subtracting the amount you still owe on your mortgage. With real-estate equity financing, a lender extends a line of credit or loan based on your equity.

Roy Rasmussen

Contributing Writer for Fast Capital 360

Roy is a respected, published author on topics including business coaching, small business management and business automation as well as an expert business plan writer and strategist.