Straight line depreciation is the simplest and most often-used formula to determine the diminishing value of physical business assets over the course of their useful lives.

We’ll look at what is straight line depreciation and why your business should use this method. We’ll also show you how to calculate straight line depreciation and take a look at the other methods of calculating depreciation to help you determine your business assets’ value.

What Is Straight Line Depreciation?

Some business assets, especially tangible assets that you can physically touch and use, lose their value as they cease to be useful and relevant (e.g., a computer system, office furniture). These are sometimes referred to as “plant assets.”

Using straight line depreciation, a linear depreciation formula, the value of an asset is reduced at a steady rate over each period until it reaches its salvage value — or the amount for which it can be exchanged when it has reached the end of its usefulness. Salvage value is sometimes referred to as “residual value” in accounting.

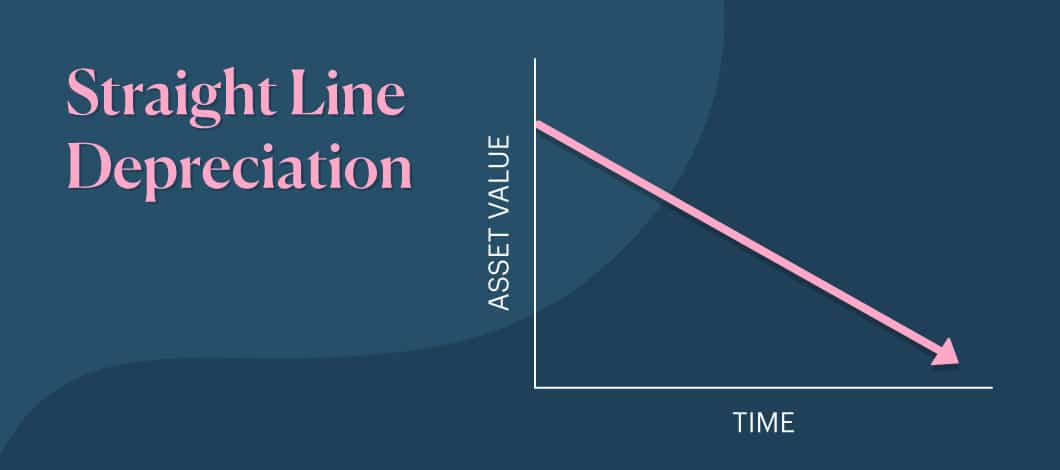

Once calculated, straight line depreciation can be represented using a simple line graph that includes a straight line, trending downward in value (y) over time (x), hence the term straight line depreciation.

How to Calculate Straight Line Depreciation

The straight line depreciation equation is the easiest method to assess an asset’s depreciation. The variables you need to input are:

- The asset’s initial cost (cost basis)

- The value of the asset at the end of its life (salvage value)

- The asset’s useful lifespan in years

Then you put the variables into the formula.

Straight Line Method of Depreciation Formula

The straight line depreciation method uses this formula:

Straight Line Depreciation = (Cost Basis – Salvage Value) / Useful Lifespan

If you purchase an asset for $3,000 and it has an approximate salvage value of $300 after 3 years, the calculation would look like this:

- ($3,000 – $300) / 3 years

- $2,700 / 3 Years

- $900 annual straight line depreciation

Your asset will depreciate by about $900 each year until it reaches the end of its lifespan, at which time it will be at its salvage value of $300.

Of course, getting the numbers to replace these variables is part of the calculation. You can estimate based on your previous experience or you can conduct research to learn about standard useful lifespans, salvage values, etc. Here is a breakdown of the variables you need:

Cost Basis of the Asset

The cost basis is the original value of your asset for tax purposes. It usually coincides with the asset’s purchase price. This is relatively easy to identify in physical assets you’ve purchased, but it can be a bit more complicated for other types of assets.

For investments, the cost basis of the asset is usually the total amount you originally invested in the asset plus any commissions, fees or other expenditures involved in the purchase. For tax purposes, it’s important to note if you reinvested any dividends and capital gains distributions rather than taking those distributions in cash. These reinvestments increase the tax basis of your investment. If you don’t account for them, you could end up paying more taxes.

Salvage Value

The salvage value is the total value of the asset when it reaches the end of its useful life. It’s the amount you could sell it for once you’re finished using it.

If your asset depreciates too much, it could reach a salvage value of $0. It’s not unusual to calculate $0 in your straight line depreciation equation because, as Accounting Coach points out, the costs to remove the asset can cancel any minimal salvage value.

Estimated Useful Life

For accounting purposes, the useful life of an asset is the number of years it can continue to contribute to revenue generation while being cost-effective.

The IRS has a useful system known as the Modified Accelerated Cost Recovery System (MACRS), which is sometimes represented as a table.

| Year | Value at Year’s Beginning | Depreciation | Value at Year’s End |

| 1 | $3000 | $900 | $2100 |

| 2 | $2100 | $900 | $1200 |

| 3 | $1200 | $900 | $300 |

Straight Line Method of Depreciation Calculator

Any calculator can handle the linear depreciation function, but you can also use a specific tool online to find straight line depreciation. You can find several of these calculators online, including at Calculator.net and CalculatorSoup

When to Use Straight Line Depreciation

While the straight line depreciation method formula is useful when determining the lifetime value of business assets, it’s also important to apply it to your tax calculations so you can maximize deductions and to your bookkeeping to keep your accounting accurate.

Tax Deductions

When you purchase an asset, you usually can’t write off the entire cost on your taxes in the year you bought it. Instead, the Internal Revenue Service (IRS) lets you deduct a portion of the cost each year over the course of the asset’s useful life.

The straight line depreciation formula will give you the same tax deduction for an asset, year after year. This works differently than other depreciation methods that provide differing tax deductions each year.

The method you use depends on the asset. IRS Publication 946 contains rules for what property qualifies for deductions and how it depreciates. For example, most farm property falls under the 150% declining balance method, while most real property falls under the straight line method.

Accounting Purposes

Because it’s the easiest depreciation method to calculate, straight line depreciation tends to result in the fewest number of accounting errors. It’s best applied when there’s no apparent pattern to how an asset will be used over time. Office furniture, for example, is an appropriate asset for straight line depreciation.

Using this method in your books lets you account for the same amount of money being taken as a depreciable business expense each year. You’ll have a better chance of keeping your accounting books clean and less chance of missing out on tax opportunities when it comes time to submit your business expenses to the IRS.

Note that part of the depreciation rate formula’s appeal is its simplicity, though a simple equation might not offer an accurate picture. The straight line depreciation equation assumes a regular decrease in value over its useful lifespan; it doesn’t account for variables that could accelerate its decline. For example, you can anticipate your computer system will degrade over the years, but an improved computer system emerging on the market can render your original system obsolete before its useful life’s predicted end.

Other Methods of Calculating Depreciation

Straight line depreciation is, in general, considered the default method for calculating the depreciation of assets. However, you can apply other methods to relevant assets and situations.

Double-Declining Balance

An accelerated depreciation method that results in a high depreciation expense in the early years, followed by gradually decreasing depreciation expenses in subsequent years. To find the double-declining balance, multiply 2 by the straight line depreciation percentage and by the book value at the beginning of the period. You’d use this method for property that depreciates faster in its first few years of use, such as a company vehicle.

Units-of-Production Depreciation

Units-of-production depreciation measures a business asset’s value decline over time and in conjunction with how much it’s used. It’s often used to assess depreciation of property such as machinery, which receives more use — and thus depreciates more quickly — in the few first years after it’s acquired. This depreciation rate formula also is best for manufacturing businesses because you consider the number of units produced when measuring value.

((Cost of Assets – Salvage Value) / Estimated Total Units Made Throughout Useful Life) x Actual Units Made = Depreciation

Sum of the Years’ Digits Depreciation

This is another method that accelerates a property’s devaluation; although it doesn’t diminish as rapidly as it does with the double declining-balance formula. To find the sum-of-the-years’-digits depreciation, add the number of years in a property’s useful life, and then divide each year by the total to find the depreciation percentage.

For example, if a piece of machinery has a 3-year useful lifespan, do the following equation:

1+2+3 = 6

Then, with the highest depreciation first, divide each year number by the total:

Year 1: 3/6= 50%

Year 2: 2/6 = 33%

Year 3: 1 / 6=17%