Looking to add a commercial truck to your business’s vehicle inventory? Unless you have a hefty cash reserve, you’ll likely need some financing.

Commercial truck loans and financing work differently than conventional car loans, making the loan application process challenging.

If you know where to look for lenders — and what they look for when judging your application — you can find the best commercial truck financing rates and get on the road in no time.

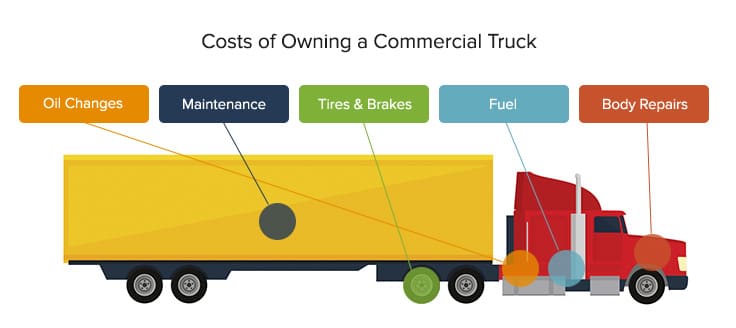

Costs of Owning a Commercial Truck

In 2021, the average trucking cost per mile in the U.S. was $2.90, accounting for such expenses as worker wages and benefits, equipment and maintenance, insurance, licensing, fuel and tires. This is considerable when you realize many truck-tractors are driven 100,000 miles or more a year.

As you can see, running a business that involves the use of commercial vehicles comes with a particular set of challenges. Commercial trucks need special upkeep, making them expensive assets for any small business.

Additionally, many of these industries (especially freight trucking) are considered risky because failure rates are high. Some lenders are hesitant or unwilling to offer in-house semi truck loans or other 18-wheeler financing.

Who Offers Commercial Truck Financing?

Large banks, truck financing companies and alternative lenders offer commercial and semi truck financing, while smaller regional banks may shy away from funding semi truck loans. Let’s look at each type of lender in detail.

Large National Banks

Although smaller chains and regional companies don’t usually take on the risk of providing semi truck financing, you can find large national banks that finance commercial trucks and trailers, such as Wells Fargo and U.S. Bank. Their resources allow them to offer low rates and long terms.

Typically, however, only the most qualified borrowers are approved by banks. If you’re looking for 18-wheeler or dump truck loans and you have bad credit, low revenues or don’t have an established business history, your chance of approval is slim.

Bank Requirements

Banks have the strictest prerequisites. Generally, you’ll need to have a good or excellent credit score to qualify. According to Experian, a 670 FICO score, a credit score reviewed by many lenders, is considered good.

Banks also favor businesses that have a long history of generating revenues. They tend to work with high-amount loans, so they need to know you’re experienced and capable of making more than enough to pay them back.

This makes it a great choice for commercial truck owner-operators with multiple years of experience. Startups and first-time buyers may need to look elsewhere.

Related: Bad Credit Business Loans? These Are Your 5 Best Options

Commercial Truck Finance Companies

Some lenders specialize in providing funding for equipment. This includes a few dedicated strictly to commercial truck and semi truck financing.

Some of the best commercial truck financing companies include the lenders listed below. Several of them even offer bad credit commercial truck financing options.

- CAG Truck Capital: Engine overhaul and semi and commercial truck financing programs

- Dostal Equipment & Financial, Inc.: Semi truck, equipment and commercial truck trailer financing

- Pedigree Truck Sales: Semi truck and semi trailer financing

- Wyatt Leasing: Equipment loans and leases for transportation, towing, agriculture, construction and waste industries

The main benefit these truck finance companies offer is their knowledge. Their experience can help you find good value in your purchase and better facilitate the deal with the seller. This leads to a smoother process overall.

However, specialized lenders, such as commercial truck financing companies, sometimes carry requirements you won’t be able to meet if you have a startup.

Truck Finance Company Requirements

Commercial truck financing lenders have their own expectations for borrowers. From credit scores to time in business, you’ll have to meet a lender’s minimum requirements to qualify for a commercial truck loan.

While specialized commercial truck financing companies aren’t as tough as banks, approval is far from guaranteed. Because they have such a handle on the trucking industry and process a high volume of applications, they might not be as likely to approve less-qualified borrowers.

Alternative Lenders

Online lenders offer fast, secure access to commercial truck loans and commercial truck fleet financing.

These lenders extend funding opportunities to business owners who are often unable to meet the requirements of banks and select equipment lenders. For this convenience, your commercial loan will likely have shorter repayment terms and higher interest rates than you’d find with a conventional lender.

If you’re seeking commercial or semi truck financing with bad credit, alternative lenders offer some of the best bad credit commercial truck loans available.

Some specialize in equipment financing for trucks and other machinery, such as National Funding and US Business Funding. In contrast, others offer a variety of financing products that you could use for any business needs.

Alternative Lender Requirements

Alternative lenders are more likely to work with you and not disqualify you from obtaining commercial truck financing for bad credit or other common reasons. This makes them an excellent option for younger businesses or business owners who are repairing their credit.

What to Know Before Applying for Commercial Truck Financing

Before reaching out to lenders, gather everything they require for a commercial truck financing application. Regardless of the lender and whether you’re looking to refinance a commercial truck loan, get commercial truck repair financing or obtain new semi truck financing, you’ll need to provide information about the vehicle, your business and yourself.

Gather Information About Your Commercial Truck

Unlike other business loans, commercial truck financing lenders need to know the exact details of the deal, including information about the seller and the vehicle.

Commercial truck financing is secured by the vehicle, making it almost as important to vet as your creditworthiness. Having all this information on hand allows lenders to judge whether it’s a smart investment for you and, by extension, them.

First, they’ll need to know what kind of commercial truck it is. This can be broken down under 2 types: vocational and long-haul (transportation) vehicles.

- Vocational trucks are single-purpose vehicles, often used in a limited geographical area. Examples include garbage trucks, ice cream trucks and dump trucks.

- Long-haul or transportation trucks are your standard semi trucks for hauling cargo across long distances.

The next thing your commercial truck financing lender will ask for is basic information about the type of truck you’re acquiring.

Be ready to provide the following:

- Year, make and model

- Vehicle identification number (VIN)

- Mileage

- Condition report (if pre-owned)

- Repair history (if applicable)

- Photos/videos

- Seller information

Generally, newer vehicles pose less risk to lenders. Mileage, of course, plays a part. For example, an 8-year-old truck with 150,000 miles may be less risky to invest in than a 4-year-old truck with 500,000 miles.

Buying from a dealer assures lenders they can trust the condition of the vehicle. Dealerships also will have more detailed repair histories that can alert you (and the lender) to any potential problems that could leave you without a truck to generate revenue.

Commercial Truck Insurance

Another cost that commercial truck financing companies take into account is insurance. Repairs and liabilities can be expensive, so lenders want to know that an accident won’t put you in jeopardy of defaulting on your commercial truck loan.

You’ll likely need to show you have insurance to obtain a commercial truck loan. Your plan may need to have the following:

- Liability coverage (including bodily injury liability)

- Non-trucking liability (for when you use the truck off-duty)

- Physical damage coverage

- Cargo coverage

- Trailer interchange coverage

Buying or leasing will determine the coverage levels you need to obtain for your commercial truck financing, but commit to a plan that balances a reasonable monthly payment with solid coverage.

-

Truck Insurance Costs

According to Progressive Commercial, their national average monthly cost for commercial truck insurance ranged from $640 for specialty truckers to $982 for transport truckers.

Submit Business Financial Documents

When applying for commercial truck financing, lenders will require documentation demonstrating you have the funds to repay your loan. You may be asked to submit the following:

- Proof of business

- Business tax returns

- Profit-and-loss statements

- Balance sheets

- Bank statements

They may also ask to see your U.S. Department of Transportation (DOT) number and motor carrier numbers from the Federal Motor Carrier Safety Administration (FMCSA).

If the lender approves of your purchase, they’ll review your documents and assess your fundability, starting with the viability of your business.

Although you could receive commercial truck financing as a first-time buyer, a history of substantial revenues and a solid business plan will afford you better commercial truck loan rates and higher funding amounts. In addition, experience in the business assures a lender that you know the industry, lowering their risk.

Add Your Personal Information

Commercial truck financing companies consider your personal history before they accept your application. Since the industry is risky, lenders need to know they can trust you to repay them.

Some things truck finance companies look for are:

- Current credit score

- Past delinquencies or bankruptcies

- Lending history

- Criminal background

Need funds to buy or repair a commercial vehicle?

Commercial Truck Loan Rates and Terms

A few factors will impact your commercial truck financing interest rates, loan terms and down payment.

Buying vs. Leasing Your Commercial Truck or Semi

The best way to finance a commercial truck will depend on your needs and specific financial situation. Keep in mind that the choice to buy or lease significantly affects the terms of your commercial truck financing or loan.

Leasing repayment terms can extend up to 5 years. Additionally, leasing carries lower monthly payments because you’re not taking out a loan on the total value of the vehicle, reducing risk to the lender. You can “buy out” a lease, but otherwise, you won’t own the truck at the end of your lease agreement.

Buying, on the other hand, typically equates to longer repayment terms and higher payments, but you’ll own the truck once the debt is paid in full.

Down Payment for Your Commercial Truck Loan

While it’s possible to be approved for commercial truck financing with $0 down and receive up to 100% of the value of the vehicle, most lenders will require a certain percentage of funds up front.

The amount of your down payment could be 10%-30%. For example, if you take out an $80,000 loan for commercial dump truck financing with 15% down, you’ll need a $12,000 down payment.

Commercial Truck Loan Interest Rates

Commercial truck financing interest rates usually fall between 5%-30%. Your rate will be based on your lender, credit history and financial health. So take this into consideration if you’re seeking bad credit commercial truck financing .

Banks typically offer the lowest rates, which can start around 5%.

Equipment and alternative lenders may start around 8% for their most qualified borrowers. If you have a low credit score and are making a riskier purchase, you could be facing a rate in the teens or higher.

Often, commercial truck loans have fixed interest rates and a set term. Repayment terms can range from 1-10 years, depending on the lender and loan.

-

Small Business Tip

Ask your lender for a complete list of the rates, terms and fees before signing. The annual percentage rate (APR) will give you a comprehensive look at how much you’ll pay in interest. Keep in mind that origination and appraisal fees are typically standard.

To estimate the cost of a commercial truck loan before meeting with a lender, check out our equipment loan calculator.

Applying for Commercial Truck Financing

Once you’ve found the perfect commercial truck and gathered all the necessary information, it’s time to apply.

If you’re applying with a bank or specialized equipment lender, you’ll need to connect with one of their loan specialists. They’ll go over your information and prequalify you for commercial truck financing before taking a closer look at your credentials. This process can take weeks, so it may not be an option if you’re in a hurry.

Online lenders can get you funding in just a few days. Through Fast Capital 360’s quick and easy application process, you can receive approvals from multiple lenders in a few hours. All you need to do is provide your business and personal financial information. Then you’ll be on your way to receiving the commercial truck financing you need to hit the road in your new business vehicle.