As with other measurements of your business’s creditworthiness, a PAYDEX score can affect your chances of getting the best rates from your creditors. We’ll explain what you need to know and how to raise your score.

What Is a PAYDEX Score?

The PAYDEX score is a business credit score provided by financial services firm Dun & Bradstreet.

It ranges from 0-100, with higher numbers showing a history and increased likelihood of a business paying its debts on time. Lenders and vendors may use a business PAYDEX score to determine loan eligibility, interest rates and repayment terms.

Even if you aren’t looking to find a small business loan or work with a new vendor at the moment, it’s crucial to understand where you fall in the PAYDEX score range and why. That way, you can increase your score and improve your odds of finding affordable funding and vendors for your business.

How Is the PAYDEX Score Used?

Your PAYDEX credit score is used by small business lenders, suppliers and vendors to determine how reliable you’ll be at repaying your debts. Business partners you want to work with also may want to check your rating before they agree to terms.

Other business entities may reference your PAYDEX score before providing their services, too. For example, if you want to rent office space or a shop, a landlord may check your score before extending a lease agreement. Or, if you require some type of business insurance, the insurer may review your score to determine your eligibility for coverage.

Your PAYDEX score does more than affect the likelihood of working with great partners. A higher score means you’re a lower-risk borrower, which can get you better terms, higher loan amounts and lower interest rates.

How Your PAYDEX Score Is Calculated

Dun & Bradstreet uses trade references to calculate and assign PAYDEX scores to businesses.

Trade references are gathered from suppliers and vendors who submit the payment histories they have with your businesses to Dun & Bradstreet. This is different from other common business credit scores since it doesn’t take into account your history with lenders and other financing institutions such as credit-card companies.

Each supplier and vendor you work with is a tradeline account, having their own transactional history with your business. Dun & Bradstreet uses the time it takes you to pay off the debts for each tradeline account to calculate your score. Let’s say a supplier sends you a $10,000 shipment of inventory. Your score will be calculated from how long it takes you to repay that debt. Paying before the due date will raise your score and look positive to future creditors.

Your score is dollar-weighted, meaning the amount and frequency of the transactions within each tradeline account factor into it. For example, the payment history with a vendor that you spend thousands of dollars with monthly will be a bigger factor in your score than a one-time transaction for a few hundred dollars.

-

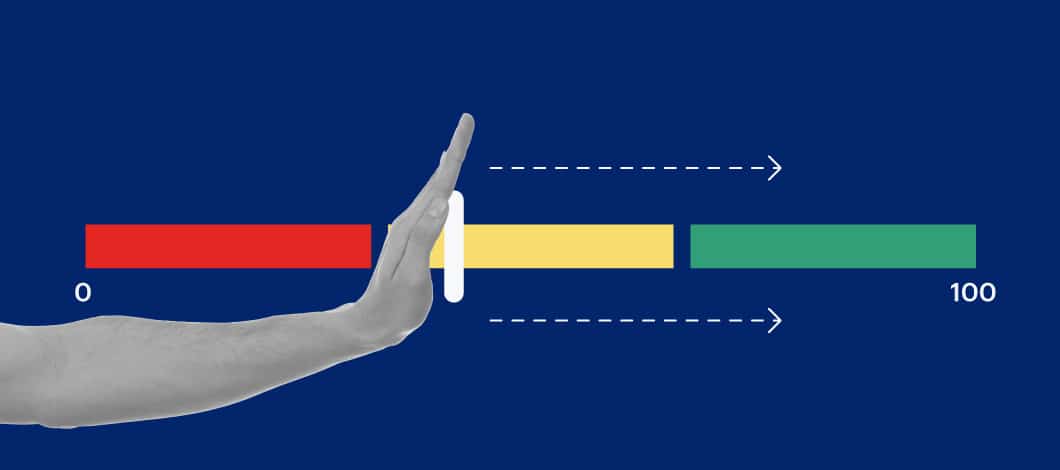

PAYDEX Score Ranges

Based on your payment histories, you’ll be assigned a PAYDEX score ranging from 0-100, with 100 being the best.

What Is a Good PAYDEX Score?

To be considered a low-risk business in relation to your PAYDEX score, you’ll want to be in the 80-100 range. A score of 50-79 indicates a moderate risk of late payment, and a score of 1-49 indicates a high risk.

Don’t fret if you aim high but don’t get above an 80. A score of 80 means you pay bills on time. You can only get a higher score by paying earlier than your terms. If you pay 20 days sooner, you can achieve a score of 90, and if you pay 30 days sooner, your score can climb to 100.

Conversely, the longer it takes you to pay your bills, the lower your score can tumble. A score of 70 indicates payments can be expected 15 days beyond terms, while a score of 30 indicates payments 90 days beyond terms.

How to Get a PAYDEX Score

To get a PAYDEX score, your business must first apply for a D-U-N-S number. This establishes your business with Dun & Bradstreet so you can become eligible for a score.

Dun & Bradstreet requires you to have at least 4 trade references to get a PAYDEX score assigned to your business. These are payments you have made to your suppliers or vendors with a payment schedule in place. That way, Dun & Bradstreet can confirm whether each payment was made early, on time or late.

Dun & Bradstreet will factor trade references from up to 875 individual business partners to determine a PAYDEX score. Trade references dating back up to 2 years will be considered, though your entire transaction history will remain on your Dun & Bradstreet file.

How to Check Your PAYDEX Score

To check your PAYDEX score, you’ll first need to purchase a business credit report from Dun & Bradstreet. They will provide free alerts to show changes in your score, so you don’t have to purchase a new report unless something has changed on your end.

Lenders, suppliers, vendors, competitors and potential business partners can purchase a copy of your credit report, as well, which is another reason why you should care about your PAYDEX score. This is what they’ll use to determine your eligibility, rates and terms for future transactions and business funding opportunities.

How to Increase Your PAYDEX Score

Increasing your PAYDEX score requires you to stay on top of your accounts and monitor what is reported to Dun & Bradstreet. Here are 6 steps you can take to increase your score in the short- and long-term.

1. Pay Your Bills Early

Always aim to pay your business bills on time, but if you can pay a few earlier, even better. Paying 10,15 or 20 days earlier on large accounts can have a significant impact on your PAYDEX rating.

2. Open Up Tradeline Business Accounts

Opening up and paying off more tradeline accounts early with your suppliers and vendors gives Dun & Bradstreet more positive data to factor into your credit rating.

3. Ask Your Suppliers to Report to Dun & Bradstreet

Dun & Bradstreet must receive vendor reports of your payments (including on-time or early payments) to calculate your PAYDEX score. There may be some vendors who aren’t reporting these transactions. Talk with your partners, especially those you do the highest-dollar transactions with and ask them to report your payments to Dun & Bradstreet.

4. Don’t Mix Personal and Business Credit

One reason why it’s critical to separate personal and business finances is that late payments you make on a business account are reported to Dun & Bradstreet—and that will affect your PAYDEX score. Let’s say you’ve made a personal purchase through a business account and you’re late making payments. Those late payments for your personal purchase will lower your score.

5. Get a Score, Even If You’re Starting Small

If your small business is still at the point where you aren’t using a lot of vendors or suppliers, you can still get a PAYDEX score. Review invoices with set payment terms for services provided by accountants, lawyers, landlords, etc. Making on-time payments to these individuals can help you establish a PAYDEX score so your business can continue to expand.

It’s also important to set up realistic payment terms with new partners. You may want to set up longer terms if possible so you can make more early payments that can bump up your PAYDEX score.

6. Sign Up for Score Alerts

Sign up for the free PAYDEX score change alerts so you can track how your efforts are affecting your credit rating. If you see something that’s inaccurate, make sure to dispute it with Dun & Bradstreet.

Make Your PAYDEX Score a Priority for Your Business

Paying your bills on time is always good business practice. It increases the trust others have in you and helps you grow necessary relationships. That’s why it’s critical to be able to show a positive PAYDEX score to potential partners, lenders, suppliers and vendors.

Make sure you apply to get a score, then take the necessary steps to increase it. Just like your personal credit score, maintaining a solid PAYDEX score can build your company’s reputation with potential partners who can help you become even more successful.