Organizing your inventory is an essential part of running a small business.

Without a good system in place, inventory management can become a nightmare to handle. If you carry too much stock, waste and costs could spiral out of control. Too little, and you won’t have the product on hand to meet demand.

Let’s cover how you can master and optimize the inventory-management process.

What Is Inventory Management?

Inventory management is knowing the quantity and location of stock you have on hand, the amount of product you need to order and when you’ll need to place orders to maintain optimal inventory levels.

Placing orders, storing products and shipping merchandise are all components of inventory management. Inventory can take the form of raw materials, works in process or finished products.

Inventory Management vs. Stock Control

Inventory control, or stock control, is part of the inventory management process that specifically concerns managing warehouse stock. Inventory control responsibilities include:

- Organizing strategic stock placement (e.g., grouping complementary items near each other to expedite order fulfillment)

- Tracking inventory location and condition

- Continuously updating stock status

Types of Inventory Management Systems

You might be wondering what kind of inventory process is best for your small business. The following are 2 inventory management types employed by businesses:

Periodic Inventory Management

As the name suggests, periodic inventory management is undertaken at designated times, such as monthly, quarterly or annually. At those times, a business counts each item in its inventory. Then the number of objects counted is compared to the number of items on record, with any discrepancies noted. Businesses also determine the costs of goods sold at this time, a figure used to calculate a business’s gross profit.

This inventory management method can be done by hand, and because no computerized inventory management system is needed, costs for implementing this type of inventory management are low.

Perpetual (or Continuous) Inventory Management

If you use inventory software or a cloud-based program and a computerized point-of-sale system, you employ perpetual inventory management. You have real-time inventory monitoring capabilities, and your inventory records and costs of goods sold are continuously updated.

When sales are made, the system updates the inventory count. Business owners can easily run reports to check stock levels and determine what needs reordering. Many modern companies use this to help streamline the steps in the inventory management process.

Inventory Management Techniques and Best Practices

With the growing importance of inventory management for small businesses, we’ve compiled a list of some popular inventory management strategies. Let’s look at several inventory management best practices.

Implement an Inventory Management System

If you don’t currently have an inventory management system, consider one to efficiently track inventory levels and improve forecasting accuracy. Having a consistently accurate count of the stock you have on hand optimizes supply ordering and reduces unnecessary costs. In fact, many inventory management systems are set up to recognize barcodes — upon scanning a product with a barcode, inventory levels are instantly adjusted to reflect the sale of the item.

There are many inventory management systems out there, and the functionality varies, so research your options before making your choice. Examples of programs that combine a point-of-sale system with inventory optimization capabilities include Cin 7 and Square. In addition, Business.org listed Fishbowl as the top option for small businesses that use QuickBooks and Veeqo as the easiest-to-use inventory management system.

Use the ‘First In, First Out’ Approach

First In, First Out (FIFO) is a strategy to ensure that the oldest products get sold first. It’s an inventory control techniques businesses that sell perishable products employ. So the next time you’re at the grocery store, check the bagged lettuce. You’ll see the bags with nearing expiration dates at the front and bags with later expiration dates behind them.

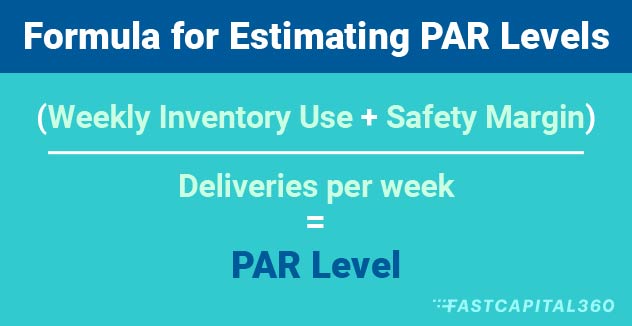

Determine Periodic Automatic Replenishment Levels

Periodic automatic replenishment (PAR) levels refer to the minimum amount of a certain product you always need to have in stock. Setting PAR levels helps prevent your company from running out of stock as well as having excess inventory. Once you set your PAR levels, you know it’s time to replenish if you fall below that number.

You can manually calculate your PAR level by taking the weekly inventory turnover and adding it to your safety stock. Then take that total and divide it by the number of deliveries per week.

Setting accurate PAR levels helps with inventory optimization. As you calculate your levels, keep the following things in mind:

- Consider order timelines and demand shifts when determining the right levels for your business.

- Having a safety margin allows your business to plan for unanticipated surges in product purchases. Review your company’s sales reports and analyze your inventory turnover speed to determine what safety margin is best to estimate your PAR level.

Apply ABC Analysis

If you’re in business, you’ve probably heard the ABC sales strategy, “Always Be Closing.” In the supply chain management world, ABC is a technique for classifying inventory items by their level of importance.

“A” items have the highest return on investment. They comprise 10%-20% of your total inventory. “B” and “C” items make up around 80% of your inventory combined: roughly 30% for “B” items, which are mid-priced products, and 50% for “C” items, the least expensive products.

Determine your “A,” “B” and “C” products so you can focus your efforts on your higher-value inventory. “A” items, for example, should never be out of stock. Due to their high value, they should also be stored in secure areas, which can help with loss prevention.

Audit Your Inventory

If you use the perpetual inventory management technique, it’s still important to conduct a physical inventory check at least once a year. While your inventory management system is likely computerized, there’s still a possibility of discrepancies, which could occur due to bar code scanning errors or theft, for example. So you’ll want to make sure you complete a manual count of your stock — often at year’s end.

Look Into ‘Just in Time’

The Just in Time (JIT) method is used by behemoth companies like McDonald’s, Dell and Harley Davidson. Depending on the industry, though, certain small businesses can consider this method too.

With this inventory process, products are made to order. As such, businesses don’t complete product or supply orders until receiving a customer order. This technique is designed to reduce waste and upfront costs you might spend purchasing and storing inventory in preparation for eventual client orders. A downside is that lead times for ordering can be impacted if supply shortages occur. For example, at the height of the COVID-19 pandemic in the U.S. in 2020, supply chains were disrupted, and businesses that use the JIT method were often short on inventory. In 2021, shipping containers are still in short supply for international deliveries, further compounding inventory availability. While many companies remain committed to the JIT method for inventory management, they’re increasing safety stock or diversifying their inventory sources to avoid stock shortages in the future.

Consider Drop Shipping

Companies that implement drop shipping have their manufacturing firms or suppliers ship orders directly to customers. This eliminates the need for the company to store inventory. Amazon sellers, for example, can employ drop shipping. When a buyer purchases a product from an Amazon seller, Amazon can fulfill the order.

Cultivate Vendor Relationships

In this digital age, it’s sometimes easy to forget that people are involved behind the scenes in our transactions. Even if you’re used to placing a supply order online, try reaching out to the company point person, particularly if your vendor is a small business owner. Who knows what benefits could come from establishing and fostering a connection?

Why Is Inventory Management Important?

Having accurate inventory information for your business can lead to improved profits, and the use of inventory management systems can provide valuable time savings. Successful inventory management can also result in the following benefits:

1. Reduced Inventory Costs

With adequate inventory control, you’ll know how much inventory you need when you need it, so you don’t over-order. In addition, placing orders according to the demand your business experiences saves money.

2. You’ll Have Products On Hand That Will Sell

If you have an inventory management system, you can analyze business reports and determine patterns when certain product sales peak. You can also track quantities sold. Use that information to ensure you have the right items in stock when you need them.

3. Customer Satisfaction Increases

With good inventory management and optimization, you have a firm grasp of available stock quantities and customer demand. Ordering stock according to your customers’ needs and wants will keep them coming back.

4. Revenue Rises

Happy customers will return and buy again. What’s more, because you’ve implemented effective inventory management, you’ll have the stock you need to help drive sales and reduce overspending. The result? More money in your business’s bank account.