Twenty-eight percent of businesses sought credit cards in 2021, according to the Federal Reserve Banks’ Small Business Credit Survey. In fact, they were the second-most desired form of financing, just after a loan or line of credit.

But what happens when your once valuable gold cards start turning into fool’s gold and leave you mining for a way out of mounting debt?

We’re letting you in on how to pay off business credit card debt and keep it off for good.

7 Strategies to Get Rid of Credit Card Debt Your Business Has Accrued

When you’re wondering how to solve credit card debt for your business, here are a few tried-and-true strategies, from settling credit card debt to renegotiating with creditors.

1. Free Up More Capital

Think about ways you can improve your revenue by cutting expenses and increasing income. This is one way to access additional funds you can apply to your outstanding business credit card balances. Just be careful to apply that increased revenue to your debt instead of spending it on your business.

2. Request Adjustments to Terms

One of the best ways to resolve credit card debt for your business is to contact the credit card company and explain you’re having difficulties keeping up with payments. Many have hardship programs and may be open to working with you.

While it may not work all of the time, some providers are amenable if you have a solid track record. They might lower your interest rate or adjust payment dates, for example.

3. Consider a Nonprofit Credit Counselor

The Consumer Financial Protection Bureau recommends that borrowers consider working with a reputable nonprofit credit counselor. These individuals may offer free educational materials and workshops as well as help you devise a plan to pay off your debt.

A couple of organizations that could help include the Financial Counseling Association of America and the National Foundation for Credit Counseling.

Note: Nonprofit credit counseling services are not the same as debt settlement companies.

-

Debt Settlement Companies

It’s advisable to avoid debt relief companies, especially those that charge upfront fees, as you can do the same thing yourself with no added cost.

Additionally, debt settlement companies will ask that you stop paying your creditors for negotiation leverage. However, this is damaging to your credit score and, again, is something you could do on your own if you find the creditor is not willing to work with you. Be mindful that the debt settlement process could take several months.

There are also many debt relief scams out there, so be wary.

If you are still contemplating working with a debt settlement company, contact your state attorney general and local consumer protection agency to see if there are any complaints against the company you’re considering.

4. Negotiate Credit Card Payoff

Another strategy is to try settling with credit card companies directly, in which you agree to pay a portion of the amount owed to satisfy the debt. While business credit card settlement is better than not paying at all, it could negatively impact your credit score and stay on your credit report for up to 7 years. Additionally, the forgiven amount could be considered taxable income when it’s time to file your taxes.

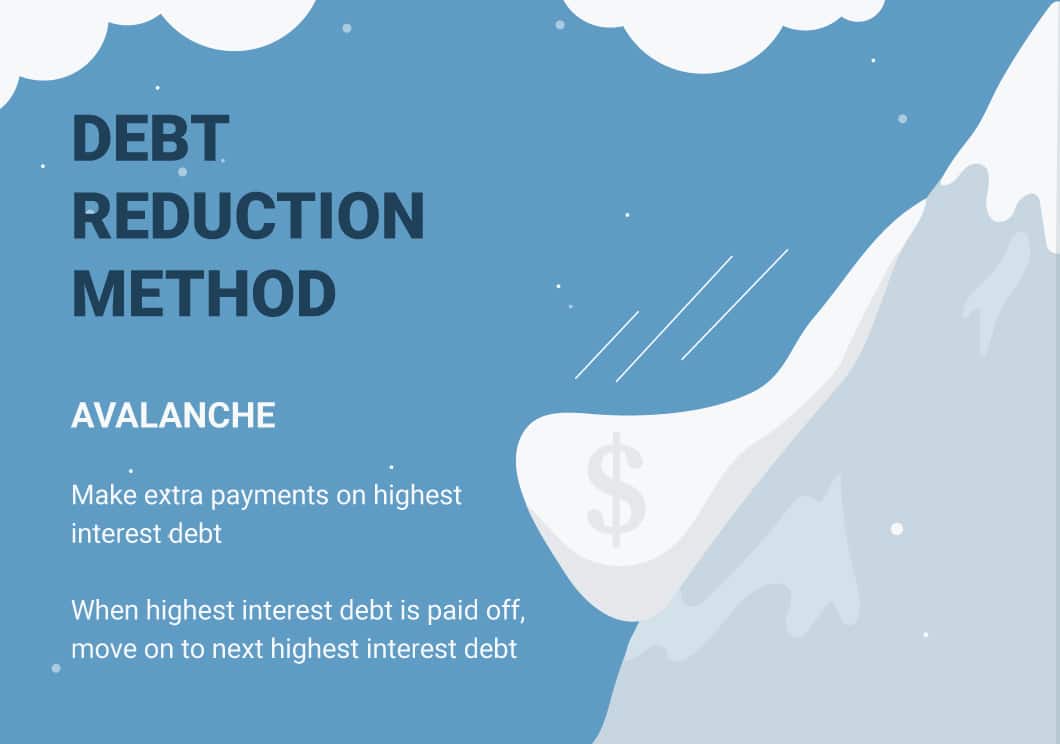

5. Use the Avalanche Method

An alternative to settling business credit card debt is to use the avalanche method. This is when you make minimum payments on all of your credit cards, except your highest-interest debt, which you put more money towards each month. The aim is to pay off your highest-interest debt first and then work your way down, applying the same payment to the next highest-rate card.

For instance, if you have a credit card with 14.99% interest, another with 20.99% and another with 24.99%, you’d start by paying off the card with the 24.99% rate first. When you pay off that card, you take the amount you were paying toward that card and apply it to the next highest interest rate card. In this case, that would be the one charging 20.99%.

All the while, you continue to make your minimum payments on your other cards. You continue in this fashion with the remaining card balances to get rid of your credit card debt.

Related: Best Strategies for Paying Off Business Debt

6. Make a Balance Transfer

If you’re wondering how to get rid of credit card debt fast, a balance transfer to a credit card with a 0% introductory interest rate could be a good option. Keep in mind you’ll likely be charged a balance transfer fee, often 2%-3% of the transfer amount or a fixed amount, whichever is greater. Additionally, if you don’t pay off the balance by the time the introductory term expires, your interest rate could skyrocket.

7. Consolidate Debt

If you have multiple credit cards, you might consider consolidating all of your business credit card debt using a single business loan. With all debts in one place, it can be easier to manage payments. Additionally, rolling all your debt into one loan could extend your terms and lower your interest rate, making it easier to handle your payments.

Want to apply for a small business loan?

How Creditors Can Collect From You

Most business credit card debt is secured by a personal guarantee, meaning if your business can’t pay, you as an individual are responsible.

For most credit card debt that goes into collections, lenders will have to file a lawsuit and get a judgment against you to recoup their losses, which is a costly and lengthy process. As such, lenders may be willing to work with you to sidestep that.

It’s important to note that creditors can pursue action against you personally to have their debt satisfied, regardless of the type of business entity you have. For example, while having a limited liability company is meant to protect you from business lawsuits, that protection does not apply when personal guarantees are involved.

Additionally, even if your company goes out of business, you can still be held personally responsible for the debt.

Why Taking Control of Your Business Credit Card Debt Is Important

Paying down your business credit cards and maintaining a good credit utilization rate and debt-to-income ratio are important in securing future financing. The lower your ratio, the better.

While it might seem challenging to stay on top of your payments today, finding a way out of mounting debt is key to improving your creditworthiness in the eyes of lenders. After all, financing is key to helping many small businesses grow. And the better your credit score, the better rates and terms you’ll receive.

How to Escape Credit Card Debt If All Else Fails

If you’ve tried every strategy to get rid of credit debt for your business and can’t find a way out, bankruptcy is an option. However, this should be a last resort, as it will drastically impact your credit for 7-10 years, depending on the type of bankruptcy you file.

Be aware that a damaged credit score will affect the availability of financing you could be eligible for in the future, as well as your terms and rates on car loans, mortgages, business loans, etc. Other side effects could include increased insurance premiums, difficulty securing leases and cash deposit requirements for utilities.

That said, you may consider the following types of bankruptcy relief:

- Chapter 11 business bankruptcy allows you to restructure your debt obligations, with approval of the bankruptcy court.

- Chapter 7 is another option. This type of bankruptcy protection requires the liquidation of your assets to clear your debts.

Additionally, while you’re going through the court process of filing bankruptcy, there is a period known as a “stay” during which the creditors you name in your petition can’t collect from you. Judgments, foreclosures and repossession of property are also suspended.

Before you decide to file any form of bankruptcy, it’s important to evaluate the benefits as well as the repercussions. Be sure to meet with a bankruptcy attorney to learn the ins and outs of what filing could mean for you personally as well as your business.