As a small business owner, building business credit to qualify for loans or financing is crucial.

If you want your business to qualify for favorable funding terms, it’s important to understand what business credit is and where your rating stands as well as how to obtain business credit. We’ll show you how to build business credit fast and improve the creditworthiness of your company.

Business Credit vs. Personal Credit

Your business credit score, like your personal credit score, demonstrates your business’s financial trustworthiness. Credit-rating firms including Equifax, Experian and Dun & Bradstreet (D&B) assign your business a credit score to tell prospective lenders how likely you are to pay your debts on time.

While some credit-rating firms will consider your personal credit score when calculating your business credit score, establishing business credit primarily depends on how well you manage your business’s financial obligations. Credit bureaus will look at several financial aspects, including business credit cards, vendor relationships, rent or lease payments as well as other outstanding debt.

Let’s take a look at the best way to build business credit, whether you’ve just begun operations or have had your doors open for years.

How to Build Business Credit for a New Business

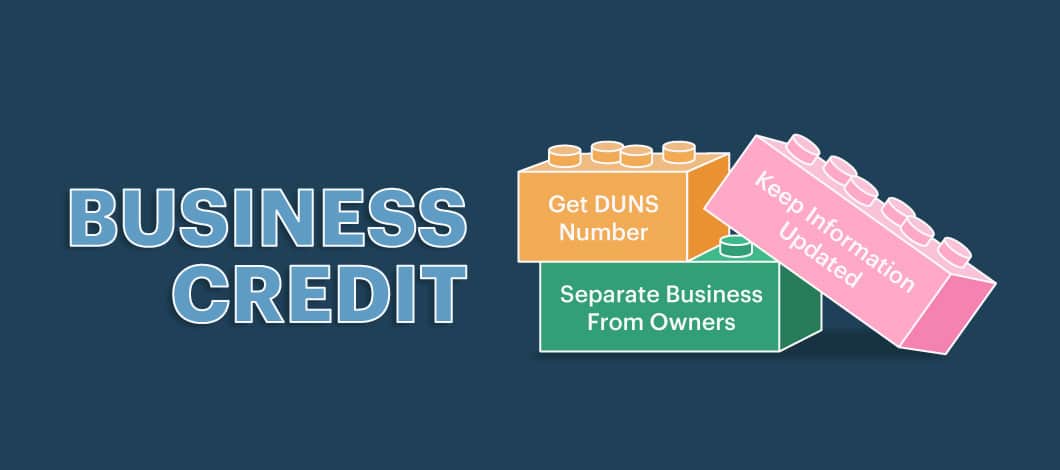

Building business credit is crucial in helping you qualify for financing. Here are 3 tips for building business credit fast:

- Separate Your Business From Its Owners

- Get a DUNS Number

- Establish and Update Your Information

1. Separate Your Business From Its Owners

First, you need to ensure that your business becomes a legal entity separate from its owners. This will protect you and keep your personal and business credit history separate.

Establishing your business credit depends on the type of business structure. For tax and credit purposes, there are 5 distinct types:

- Limited liability company (LLC)

- S corporation

- C corporation

- Sole proprietorship

- Unincorporated business entity

If you want to open a business credit file, consider structuring under any of the first 3 models. Under these arrangements, your personal credit score is kept financially and legally distinct from your business credit.

Take this time to obtain a business tax ID, also known as an employer identification number, if applicable. Additionally, open a business bank account if you haven’t already.

2. Get a DUNS Number

Applying for a Data Universal Number System (DUNS) number is essential for establishing business credit. Registering for this 9-digit identification number — developed by Dun & Bradstreet — is free, but it may take as long as a month to be processed.

Having a DUNS number isn’t mandated by government legislation, but it’s required to open a credit file with Dun & Bradstreet, a top credit-rating firm. You also will need a DUNS number to apply for government grants and contracts.

What Are the Business Credit Reporting Agencies?

The following are 3 major credit-rating firms:

Open a business credit file with each of the firms. The file includes data a credit-rating firm collects on your business and credit-management history.

Your business credit file includes your name, address and credit inquiries as well as the payment history between your small business and vendors, banks, lenders and others.

3. Update Your Information

As a business owner, it’s crucial to keep your information current with credit bureaus. This includes details such as years in operation, the number of employees and financial documents.

Keep in mind each credit-rating firm uses different scoring algorithms, meaning your small business could receive other scores. Maintaining up-to-date information with all 3 of the major credit-rating firms is imperative for business owners because each firm carries a slightly different picture of your business, and a lender or supplier could check your credit report from any of the 3.

Also, note that some vendors might report to some firms and not others.

-

How Long Does It Take to Build Business Credit?

Advice varies in this area, with some sources claiming several months while others say it could be 3 years. How long you’ve been in business and your current credit score are considered when establishing your business credit.

How To Build and Maintain Business Credit

- Be Consistent

- Pay Your Bills on Time

- Maintain Your Personal Credit Score

- Keep Your Business Credit Diverse

- Monitor Your Credit

1. Be Consistent

Building business credit is about playing the long game. Maintaining the same physical address, company name and telephone number on all public records, registries and correspondence can go a long way in establishing your business entity’s permanence and longevity in the eyes of lenders.

In turn, your consistency pays off in the form of credibility.

2. Pay Your Bills on Time

To build business credit fast, promptly pay your bills. Just as with personal credit, late payments will hurt your scores. If you can manage it, paying your vendors early is one of the best ways to build business credit.

Remember: Work with vendors that report payments. Otherwise, your credit-building efforts could go unnoticed.

3. Maintain Your Personal Credit Score

Although your business’s credit is a legally separate entity, it’s crucial to maintain a good personal credit rating, too. This is because lenders will still consider your personal credit score as they evaluate how you manage your debt obligations.

Lenders will also check the credit scores of all your shareholders when it comes time to secure financing. Shareholders with more than a 20% stake can expect lenders to check their personal credit rating.

4. Keep Your Business Credit Diverse

As you’re building business credit, broaden your profile to include accounts from multiple creditors. This could include:

- Vendor lines of credit

- A business credit card, such as:

- An LLC credit card

- A personally guaranteed business credit card

- A business line of credit

Applying for a secured business credit card arguably can be the fastest way to build business credit. This is because a deposit backs secured credit cards — for instance, a deposit of $1,000 qualifies you for a credit limit of an equal amount.

It’s more challenging to qualify for an unsecured business credit card, as they don’t require a deposit or collateral.

When you diversify your credit, your company’s creditworthiness gets a lift in the eyes of creditors.

5. Monitor Your Credit

You can keep an eye on your business credit by taking advantage of software, some of which is free, that automatically notifies you whenever your credit rating changes. Use these tools to address any sudden changes to your business credit.

Another benefit of keeping close tabs on your business credit score: Detecting possible identity theft.

Companies That Help Build Business Credit

In addition to your efforts to pay bills on time and diversify your credit, you can work with companies that help build business credit. There are 2 main options for you:

Net 30 Vendors

A net 30 account allows businesses to purchase items or services and pay off the balance within 30 days. Net 30 vendors who offer these accounts and report to credit agencies can help you get business credit. Some net 30 vendors include the following companies:

Consultants

A consultant can review your current obligations and credit score and make recommendations to improve them. Keep in mind that you’ll have to pay for these services. Some consultants, such as Fund&Grow, offer consulting as well as funding access in a business credit-building membership program.